搜索

Institutional Capital Dispatches: April Equity Regimes and Multi-Factor Asset Allocation via Arakawa Quant

Executive Summary

Macro Milestone: Global equity markets concluded April with their most robust monthly performance since 2020. Driven by record-breaking hyperscaler capital deployment commitments, the S&P 500 achieved unprecedented historical territory, while the Nasdaq Composite decisively violated the 25,000 threshold.

The $700 Billion Catalyst: Comprehensive financial disclosures from mega-cap tech networks—specifically Microsoft (MSFT), Alphabet (GOOGL), Amazon (AMZN), and Meta Platforms (META)—confirmed an aggregate projected AI infrastructure capex expansion surpassing $700 billion, establishing an aggressive fundamental runway for supply-chain executors.

Fixed-Income Crosscurrents: WTI crude’s transient breach of the $100/barrel threshold reignited late-cycle inflationary anxieties, driving the benchmark 10-Year U.S. Treasury yield ($$US10$$) back above 4.40% and cementing restrictive baseline policy expectations for the remainder of the 2026 calendar year.

Systematic Outperformance: The Arakawa Quant multi-factor model continues to extract persistent structural alpha, securing an absolute return of +348.72% since inception, compared to +90.38% for the S&P 500 index, by screening out behavioral biases and concentrating on high-visibility earnings execution.

Macro Regime Layering: Hyperscaler Capex and Fixed-Income Volatility Vectors

The closing interval of April marked an extraordinary capital expansion phase across broad equity benchmarks. The foundational driver of this thematic tailwind was the unprecedented mobilization of balance sheet liquidity toward artificial intelligence computing architectures. Earnings data compiled from four dominant technology nodes confirmed a multi-year capital deployment mandate totaling over $700 billion. This immense capital influx has fundamentally altered the structural demand curve for technical data center networks, rendering near-term seasonal anxieties (e.g., historical "May seasonality") mathematically secondary to the structural earnings velocity of growth assets.

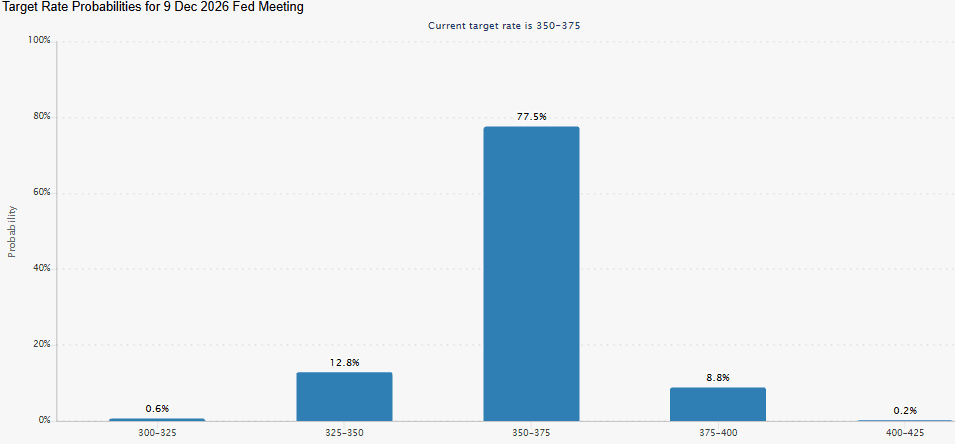

FedWatch Tool, CME Group

Conversely, the macroeconomic landscape presents complex crosscurrents within the fixed-income and commodity complexes. Supply-side frictions, primarily linked to Middle Eastern geopolitical developments and naval transit vulnerabilities through the Strait of Hormuz, drove crude oil prices above $100 per barrel earlier in the period.

The fixed-income curve reacted swiftly to this energy-driven inflation proxy, forcing the 10-Year U.S. Treasury yield ($$US10$$) to climb past 4.40%. This shift indicates that financial conditions will likely remain tighter for longer, as central bank policy frameworks maintain restrictive mandates to anchor core inflation expectations. A sustained de-escalation in commodity pricing remains the primary prerequisite for near-term valuation expansion across defensive equities.

Sector Rotations & Factor Dispersion Metrics

Reflecting these macro crosscurrents, equity markets exhibited intense sector dispersion throughout the month:

Technology (XLK): Emerged as the dominant sector allocator, propelled by expanding corporate operating margins and unprecedented backlog visibility across the AI hardware and optical infrastructure stack.

Consumer Discretionary (XLY): Documented persistent capital inflows, sustained by resilient high-income household balance sheets within a highly pronounced K-shaped macroeconomic architecture.

Defensive De-allocation (XLV / XLE): Healthcare (XLV) underperformed due to lingering regulatory policy uncertainties and muted near-term earnings growth. Energy (XLE) retraced late in the month as a minor technical de-escalation in crude oil spot prices muted short-term earnings revision momentum.

Arakawa Quant Multi-Factor Edge & Micro-Cap Performance Attribution

To systematically harvest alpha from this high-dispersion regime, the Arakawa Quant engine relies on a strict rules-based filtration across five mathematical pillars: Valuation, Growth, Profitability, Momentum, and Earnings Estimate Revisions. This mathematical isolation preserves portfolio integrity against headline-driven behavioral volatility.

Weekly Portfolio Performance Attribution:

Positive Factor Contributors (Accelerated Core Fundamental Scaling):

TTM Technologies (TTMI): Surged after delivering a significant Q1 earnings beat and upwardly revised forward guidance, driven primarily by inelastic procurement of high-density multi-layer printed circuit boards (PCBs) across AI data center and high-tier networking markets.

Micron Technology (MU) & Lumentum Holdings (LITE): Both registered substantial gains, demonstrating powerful factor momentum within the high-bandwidth memory (HBM) and optical transport network infrastructure supply chains.

Powell Industries (POWL): Benefited from a supply-demand mismatch in grid-level high-voltage electrical equipment triggered by nationwide data center expansion, extending corporate order visibility out multiple quarters.

Brinker International (EAT): Achieved significant outperformance capture within the consumer discretionary quadrant, sustained by superior brand equity resilience and exceptional high-frequency restaurant foot traffic.

Negative Factor Laggards (Technical Distortions & Near-Term Margin Pressures):

Vistance Networks Inc. (VISN): Declined sharply on an optical basis, representing a purely mechanical adjustment rather than fundamental deterioration, as a $10 special cash distribution triggered an equivalent pricing reset on the ex-dividend date.

Wayfair Inc. (W): Retrenched as minor fluctuations in high-frequency credit card data generated short-term institutional caution regarding the durability of the big-ticket home furnishings retail recovery.

SkyWest, Inc. (SKYW): Faced transient operating margin compression as a brief spike in crude oil prices toward triple digits introduced elevated aviation fuel cost frictions.

Credo Technology Group (CRDO): Experienced a technical sympathy correction, tracking sector-wide sentiment contagion after peer provider POET Technologies plummeted approximately 47% on isolated purchase order cancellations.

Kinross Gold Corporation (KGC): Consolidated as spot gold pricing momentum stabilized alongside flattening benchmark Treasury yields, prompting late-cycle profit-taking across the precious metals mining complex.

Institutional Asset Allocation & Portfolio Governance

Managing institutional capital against midyear macroeconomic volatility requires a deliberate transition out of passive, cap-weighted indexing and into data-driven factor modeling. Utilizing an equal-weighted, rules-based mandate across nearly 5,000 U.S.-listed equities and ADRs provides institutional allocators with a diversified framework to extract volatility alpha while eliminating single-stock concentration risks.

By continuously optimizing portfolio exposure for high earnings visibility, balance sheet safety, and factor purity, the Arakawa Quant architecture ensures that deployed capital captures structural technological transformations while remaining insulated from broader macroeconomic shifts.