搜索

Quantitative Decisions Amid Macro Storms: Arakawa Core Portfolio Weekly Recap & Deep Multi-Factor Strategy Analysis

Executive Summary

Risk-Off Rotation Sweeps U.S. Equities: An escalation in Middle East geopolitical tensions, coupled with stubborn inflation stickiness and hawkish expectations of a Federal Reserve keeping rates "higher for longer," collectively cooled market bulls. The S&P 500 now faces downward pressure to snap its impressive nine-week winning streak.

AI Chip Sector Suffers High-Valuation Pullback: Despite a blowout earnings report from Broadcom (AVGO), a classic "sell-the-fact" wave triggered widespread profit-taking. This rapidly evolved into a sector-wide correction across semiconductor and AI infrastructure plays, temporarily halting the fierce rally seen this quarter.

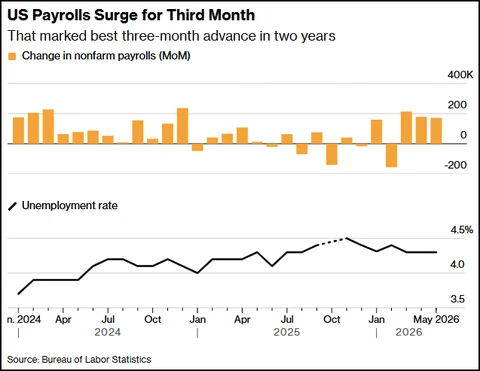

Nonfarm Payrolls Highlight Economic Resilience: U.S. nonfarm payrolls for May surged well ahead of consensus estimates, while the unemployment rate held steady at 4.3%. A tight labor market reinforces the higher-rate macro backdrop, prompting the Fed to remain highly prudent on its rate-cut trajectory.

Volatility as a Prime Contra-Trend Entry Window: Historical data demonstrates that while short-term, catalyst-driven shocks shake the confidence of discretionary traders, they create structurally attractive contrarian entry points for Arakawa’s fundamentally backed quantitative stock-selection framework.

1. Macro Perspective: Risk-Off Shocks Accelerate as Semiconductors Consolidate

Following weeks of relentless upward momentum, U.S. equity markets saw a pronounced deceleration this week. The causal chain behind this correction stems from an intersection of macroeconomic data points and geopolitical risk factors. Midweek, renewed flare-ups in the Middle East—specifically involving Iran-backed factions—sent international energy prices and market anxiety higher. This friction cross-reverberated with persistent, sticky inflation anxieties, forcing Wall Street to reprice the Fed's monetary path: "higher for longer" is no longer just a cautionary warning, but the central baseline for asset pricing. The S&P 500 is currently on track to log its first weekly decline of the quarter, testing the resilience of its nine-week bull run.

This institutional risk-off rotation culminated on Thursday, sparked by tech bellwether Broadcom (AVGO). On a purely fundamental basis, Broadcom delivered a blockbuster earnings print, featuring record-high revenue, robust net margins, and solid forward guidance. However, within an overcrowded semiconductor trade, this flawless report ironically triggered heavy "sell-the-fact" liquidation. Broadcom’s intraday slide quickly generated a domino effect, dragging down semiconductor peers and prompting a broader valuation haircut across mega-cap tech.

Arakawa Market Breadth Assessment: While short-term selling in tech heavyweights placed obvious pressure on the market-cap-weighted indices, an examination of internal market breadth reveals a healthy, structural rotation. Approximately two-thirds of S&P 500 constituents actually advanced this week. Concurrently, the Dow Jones Industrial Average pushed closer to its all-time highs. This divergence indicates that capital is not fleeing equities in a panic; rather, it is executing a rational reallocation away from overextended, highly concentrated AI leaders and into resilient cyclicals and defensive value plays.

Friday’s highly anticipated May nonfarm payrolls report provided the definitive macro capstone for the week. Job gains dramatically outpaced consensus forecasts, spearheaded by robust hiring in leisure and hospitality, healthcare, and the government sector. Crucially, construction and manufacturing also exhibited sustained expansion—二 cyclical areas continuing to harvest the capital expenditure (CapEx) boom driven by AI data center buildouts and supply chain reshoring initiatives.

With the unemployment and labor participation rates holding remarkably steady at 4.3%, the domestic labor market remains sufficiently tight to give the Fed ample leeway to maintain its restrictive policy stance. Following the data release, Treasury yields—particularly the policy-sensitive short end—shot up across the curve, and the swaps market began modestly pricing back in the tail risk of an additional rate hike later this year.

2. The Arakawa Quantitative Edge & Active Portfolio Dynamics

During intense periods of market churn, discretionary asset management frequently succumbs to behavioral biases, resulting in emotional panic selling or premature bottom-fishing. Arakawa Quant eliminates human emotion entirely through a disciplined, systematic factor model. Our quantitative algorithm targets high-conviction equities utilizing five primary underlying criteria: Valuation, Growth, Profitability, Momentum, and Earnings Estimate Revisions.

This quantitative discipline has reliably engineered superior long-term outperformance (Alpha) across market cycles:

Cumulative Alpha: Since the algorithm's inception, the master Arakawa Quantitative Portfolio has generated an exceptional cumulative return of +439.91%, substantially outperforming the S&P 500’s return of +100.56% over the identical period.

Compounded Winners: Within our active portfolio matrix, 17 distinct positions (representing 15 individual equity tickers) have already locked in returns exceeding 100%.

Alpha Resilience: Despite the sector-wide semiconductor drawdowns, the total portfolio's downside was heavily insulated, with three core long holdings gaining more than 20% this week alone.

While short-term sector pullbacks of 15% or more can be psychologically challenging for self-directed investors, Arakawa's quantitative research team has tracked over 15 years of comprehensive performance history for top-tier systematic equities during historical market declines:

"Investors who methodically acquired the top 10 Arakawa Quant 'Strong Buy' stocks following a broader market drop of 15% or more, and held those positions for a fixed two-year horizon, achieved average absolute gains of 117%—more than double the S&P 500’s performance over the identical time frame."

This statistical backtest highlights that when elite, fundamentally sound equities are temporarily discounted due to systemic market-wide beta corrections, it routinely represents a premium buying window for multi-factor models.

3. Algorithmic Breakdown: Demystifying Arakawa’s Rebalancing via Royal Caribbean (RCL)

Over the past several weeks, our customer support and quantitative research divisions received numerous inquiries from our subscription community regarding the systematic rebalancing of Royal Caribbean Cruises Ltd. (RCL). This specific transaction serves as an air-tight demonstration of our algorithmic logic:

The Initial Profit Realization (Last October): Following a powerful, multi-month upward expansion, RCL triggered our automated "Winner Realization Protocol" as its Valuation and Momentum factors hit cyclical overbought targets. The position was systematically liquidated to crystallize substantial accumulated Alpha.

The Quantitative Re-Qualification: Following that exit, as Royal Caribbean reported subsequent quarterly earnings filings, its core Profitability and Growth factor metrics experienced real-time upward adjustments. The stock completely re-qualified under our strict multi-factor criteria. Consequently, the algorithm un-emotionally re-entered the position, initiating a fresh, standard 180-day holding cycle.

Arakawa Core Risk Philosophy Clarification: We want to take this opportunity to explicitly remind our investment community that Arakawa's foundational mandate is to "Let Your Winners Run." Throughout the duration of any asset's initial 180-day holding period, the system enforces a strict holding rule, barring any catastrophic fundamental deterioration.

The Arakawa Quant team is currently finalizing a rigorous, high-dimensional multi-factor backtest and stress-testing module centered entirely on “post-180-day holding criteria optimization.” This research focuses on refining our transition metrics to minimize unnecessary turnover during volatile sideways markets. A formal system architecture update will be delivered across our web and mobile applications immediately upon successful validation.

4.Advanced Portfolio Optimization: Implementing the Barbell Strategy

In highly unpredictable macroeconomic environments, maintaining a monolithic investment style exposes a portfolio to intense drawdown risks. Arakawa strongly advocates the implementation of a disciplined Barbell Strategy in the current market climate:

The Growth End of the Barbell (Attack): Allocate to high-velocity, high-alpha Arakawa core quantitative growth selections. Backed by exceptional earnings visibility, these names act as capital compounders during market upswings.

The Defensive End of the Barbell (Defense): Anchor the portfolio with highly stable, cash-flow-generative dividend assets. Currently, the dividend-paying constituents embedded within the Arakawa framework deliver an average forward dividend yield of 1.43%, significantly outperforming the S&P 500’s baseline of 0.95%. This reliable stream of defensive yield provides an essential buffer against systemic capital drawdowns.

Conclusion & Outlook

Looking into next week, global financial markets face their most critical macroeconomic catalyst of the month: the release of the newest CPI (Consumer Price Index) report. This specific data point will directly dictate interest rate policy expectations, reset institutional risk tolerances, and determine how rapidly global capital rotates back into growth equities and secular AI infrastructure leaders.

In an era of macro storms, objective data is the ultimate equalizer. Arakawa Quant remains resolutely dedicated to providing a mathematically rigorous framework designed to strip emotion out of wealth compounding.