First

Last

email@email.com

Quantitative Stock Analysis: A High-Gear Semiconductor Supplier Riding the AI Growth

Arakawa Quant Picks

July 1, 2026

Skye

Decoding institutional Liquidity Sweeps

Summary

- This company is a critical upstream supplier to the semiconductor industry, giving it a mission‑critical role in chip quality, yield, and reliability.

- Revenue is growing at a double‑digit rate, and our quantitative system notes that management expects every quarter of 2026 to show further growth as AI spending ramps up.

- Profitability continues to improve as higher volumes boost factory efficiency and more production shifts to lower‑cost plants and in-house-branded parts.

- Based on the ArakawaQuant Factor Model, the stock has demonstrated powerful price momentum and rising earnings estimates, while still trading at a discount across key valuation metrics.

Business Overview

As a top Quant-rated asset within our equity selection universe, Ichor Holdings (NASDAQ: ICHR) designs and manufactures fluid delivery subsystems for semiconductor manufacturing equipment. The company acts as a critical upstream supplier to leading semiconductor equipment manufacturers like Applied Materials (AMAT), Lam Research (LRCX), and ASML (ASML).

Ichor’s subsystems sit inside chip‑making tools and manage gas and chemical flows for etching, depositing, cleaning, polishing, and plating silicon wafers. Their role is to deliver and precisely control specialty gases and liquids, which directly affect chip quality and yield. Errors in these flows can ruin an entire batch of wafers, so equipment makers and chip fabricators place a premium on reliability. That focus on dependable performance gives Ichor pricing power and differentiation from a typical commodity parts supplier.

The company’s main products include gas delivery systems for etch and deposition tools and chemical delivery systems for CMP (chemical mechanical polishing), electroplating, and wet cleaning. Ichor sells primarily to semiconductor equipment manufacturers; as such, its revenue benefits from capital‑spending cycles at major logic and memory chipmakers. Growing AI demand increases the number and complexity of etch and deposition steps, which raises the need for sophisticated gas and chemical control. As designs shift toward architectures such as gate‑all‑around (GAA), process steps multiply, and recipes become more intricate, expanding the amount of Ichor content per tool.

Beyond semiconductors, Ichor applies its engineering and manufacturing capabilities to the aerospace, defense, and medical markets, helping diversify the company's customer base beyond semiconductors. Headquartered in Fremont, California, Ichor operates globally and is expanding its manufacturing footprint, including Mexico and Malaysia, to lower costs and vertically integrate.

Our Quantitative Buy Thesis

From our systematic research perspective, Ichor offers a technical niche with limited direct substitutes, making it a mission-critical partner for original equipment manufacturers (OEMs) that need reliable, high-performance fluid delivery. The company has benefited from surging AI-driven capex, and its Q1 2026 results suggest that the tailwind is strengthening. Management now expects every quarter in 2026 to be a growth quarter, and double-digit sequential growth to be anticipated in the second half. Industry-wide transitions in semiconductor architecture are helping drive Ichor's growth:

“A great example of this is the 30% increase in the number of process steps required to produce leading-edge logic with gate-all-around architectures. Increased investments in gate-all-around technology are significant tailwinds for Ichor's growth,” said Phil Barros, CEO of ICHR.

Ichor’s business model centers on close co-development with OEMs on platform-specific subsystems that are costly to redesign once implemented, creating high switching costs and supporting revenue stability.

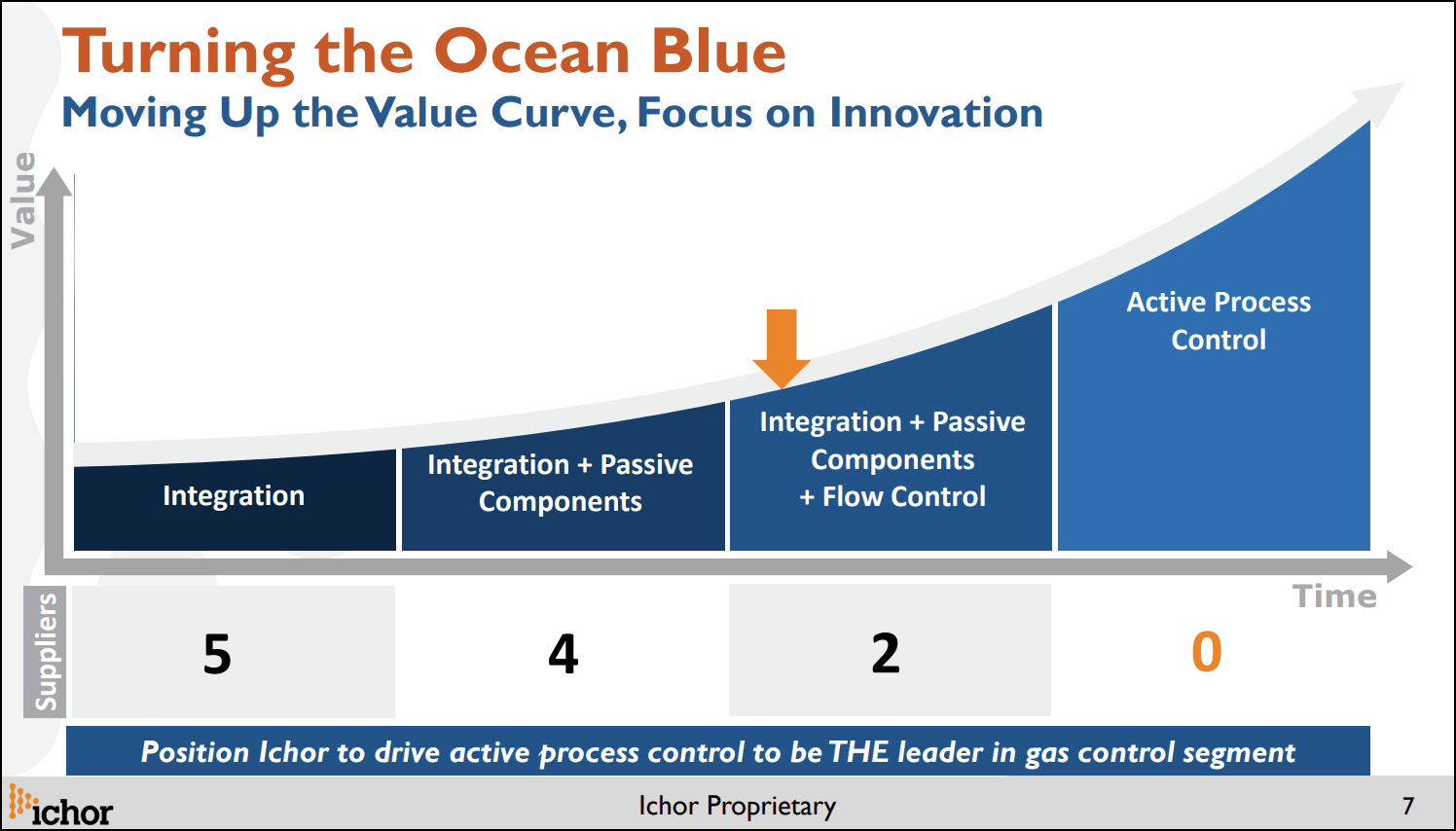

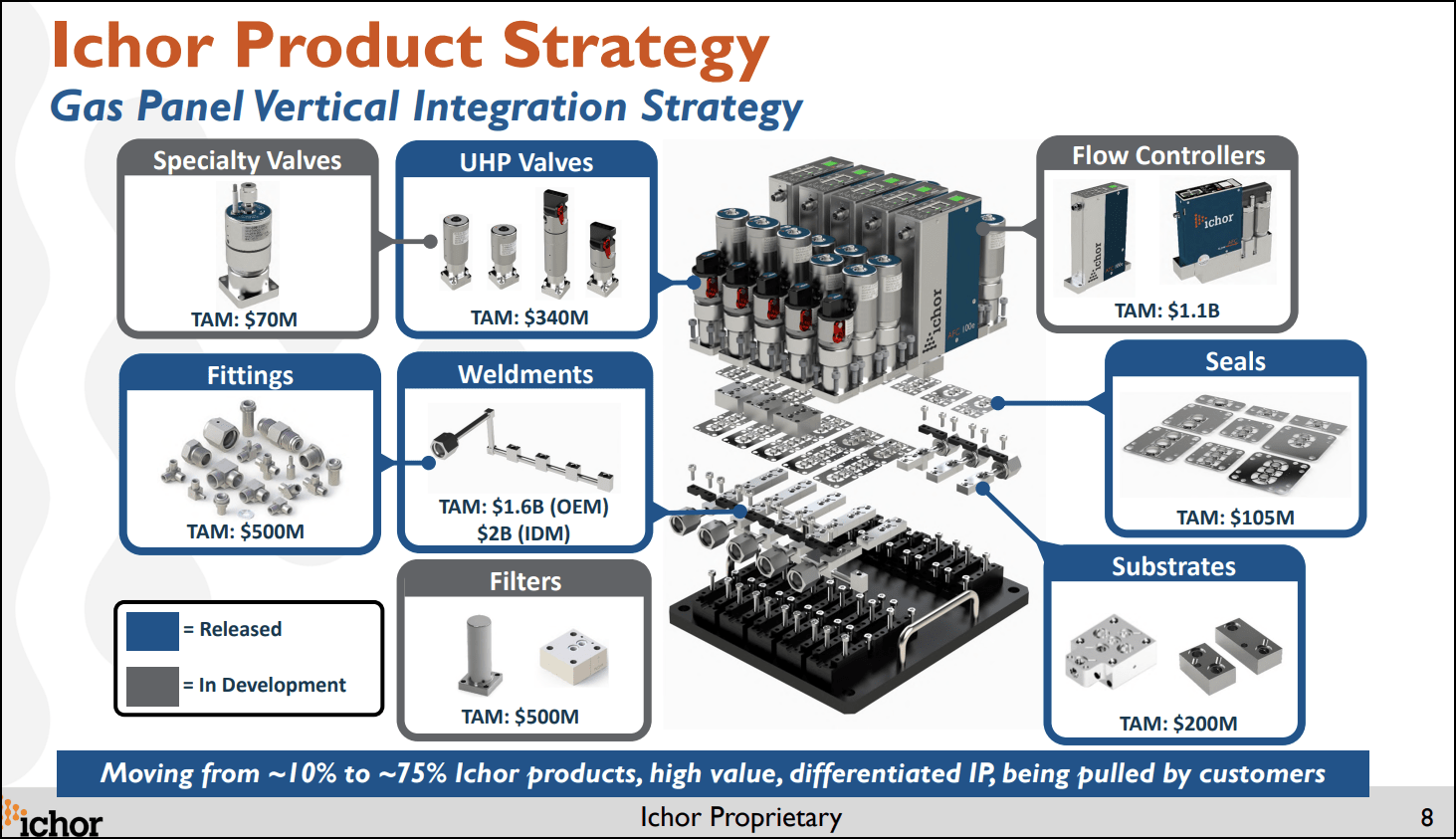

Importantly, Ichor continues to shift toward a more vertically integrated model with proprietary, Ichor-branded content. Branded content rose from 15% of systems in 2024 to 25% in 2025, and management reiterated a year-end 2026 target of 35%, with the capability to reach up to 75%. This mix shift is a primary lever behind the company's near-term gross margin target of at least 15%, with management guiding roughly 100 basis points of margin expansion per quarter through the second half of 2026. With the AI capex cycle still in its early stages, restructuring efforts ahead of schedule, and its product mix continuing to shift toward higher-margin proprietary components, Ichor offers strong potential for long-term quantitative alpha.

Our internal factor grading engine evaluates a stock's investment characteristics relative to its industry peers. Based on the data model below, ICHR scores exceptionally well across growth metrics, as well as important timeliness indicators like momentum and earnings revisions. Below, we'll detail aspects of the company's profitability and valuation to understand where it ranks among other semiconductors.

ICHR Growth and Profitability Factor Analysis

Revenue Performance in the Early Stage of an Explosive Phase:

Ichor’s Q1 2026 financial performance confirms that the company is in the early innings of a powerful growth phase. Quarterly revenue rose 15% sequentially to $256.1 million, landing at the high end of guidance and reflecting stronger-than-expected demand across core wafer fab equipment markets. Q2 revenue guidance was further raised to $290–$310 million, signaling a robust sequential surge of roughly 17%. Meanwhile, the company is already installing and qualifying its overseas manufacturing transitions ahead of schedule, which not only supports near-term capacity needs but also aligns with its long-term growth ambitions. From a quantitative perspective, the company showcases excellent near- and long-term FWD EPS growth, clocking in at 761% and 275% above the sector median, respectively.

Gross Margin Inflection Point and Two Core Drivers:

Following a weak earnings stretch, Ichor’s profitability is turning a crucial corner. The company delivered a sharp improvement in Q1 2026 operational performance, with gross margin expanding 110 basis points sequentially to 12.8%. This expansion helped operating income more than triple compared to Q4 and drove the highest EPS in three years. This improvement stems primarily from two core forces: first, higher volumes are helping the company use its factories more efficiently to better absorb fixed manufacturing costs; second, a set of longer-term structural changes—shifting more production to Mexico and Malaysia and increasing the share of higher-margin Ichor-branded components—are expected to add roughly one percentage point of gross margin each quarter through the second half of 2026.

Strict Discipline in Fixed Costs:

Complementing these operational efforts is tight cost discipline; despite a double-digit revenue ramp, operating expenses (OpEx) were held to only mid-single-digit growth.

Correction of Backward-Looking Financial Factor Lags:

Standard accounting profitability metrics are typically backward-looking, and the rolling historical grades still reflect Ichor’s previous weak earnings stretch. However, our real-time profitability factor model indicates that its score has already moved up significantly from three months ago. Furthermore, its above-average asset turnover and healthy capex-to-sales ratio indicate efficient use of its asset base and a disciplined growth investment style.

Earnings Revisions, Momentum, and Valuation Matrix

Confidence in Ichor’s profitability turnaround is echoed by Wall Street analysts: the company has received unanimous upward earnings revisions over the last 90 days versus zero downward, highlighting conviction in its business model and execution from a consensus perspective.

The company has sustained exceptional price momentum over the last four quarters, which, alongside strong fundamentals, acts as a powerful predictive indicator within our mathematical models for future returns. It’s important to note that semiconductor stocks have swung sharply over the past couple of weeks, with a broad selloff tied to macro profit‑taking. After that pullback, many names have bounced over the last few sessions as investors step back into the group, reflecting ongoing conviction in the long‑term AI and data‑center build‑out. Some of the more sizable moves have been found among equipment manufacturers. Ichor and its peers have posted strong gains over the past week, with ICHR’s share price move reflecting broader market volatility rather than a change in its fundamental story.

The stock still trades at a significant discount on key valuation metrics, including a FWD PEG that is 16% below the IT sector median, presenting a highly attractive entry setup for systematic strategies.

Potential Risks

Ichor faces customer concentration risk, with a small number of large semiconductor equipment manufacturers driving a substantial share of its revenue. Pauses in AI capex or broader macro weakness can compress orders and margins. Supply chain and operational risks are also important. Ichor relies on the timely availability of specialty components, metals, and process consumables. Disruptions, cost spikes, or quality issues at suppliers can delay deliveries and impact profitability.

As the company scales manufacturing across geographies, it faces execution risk around ramping up new facilities, maintaining consistent quality, and managing labor availability and costs. Finally, competitive and technology‑transition risks matter: equipment makers can redesign tools to reduce Ichor content, shift to competitors, or adopt new process technologies that require different solutions, potentially pressuring pricing power and market share.

Concluding Summary

Ichor’s growth is being driven by surging AI‑related capital spending, more complex wafer‑fab processes, and a rising mix of proprietary, Ichor‑branded subsystems that deepen its content in leading‑edge tools. Its fluid delivery systems are integral to the AI build‑out because every advanced logic and memory chip used in data centers relies on tightly controlled gas and chemical flows in their manufacturing, making Ichor’s modules mission‑critical. Recent quarters highlight both strong top‑line acceleration and a clear profitability inflection, as higher volumes, vertical integration, and low‑cost manufacturing in Mexico and Malaysia push margins higher. Together with strong price momentum, unanimous upward earnings revisions, and a forward PEG ratio still well below the sector median, ICHR is systematically positioned for long-term outperformance.

The ArakawaQuant Core Selection Matrix mechanically monitors thousands of liquid U.S. equities based on real-timefactor health. Click the link below to access our institutional-grade quantitative portfolio dashboards and automated execution models.

In an era of information overflow, alpha lies in asymmetric execution, not intuitive consensus

Skye

SMC Market Analyst

Subscribe to our newsletter

Get the insider insights you need to scale, straight to your inbox.

Decode the Market. Quantify Your Edge.

Elite quantitative models and real-time execution signals. Trade with institutional power.

Copyright © 2026 Hong Kong Arakawa Limited. All rights reserved.

%2C%20Color%3DNegative.svg)