First

Last

email@email.com

StoneX (SNEX) Monopolizes Commodity Risk Intermediation as Q2 Net Income Surges 143%

Arakawa Quant Picks

June 17, 2026

Ada

Liquidity Architect & Institutional Order Flow Analyst

Executive Summary

- Systematic Positioning: StoneX Group Inc. (SNEX) operates as a premier global institutional-grade financial intermediary, connecting real-economy commercial producers, mid-market corporations, and institutional traders to specialized liquidity networks often underserved by tier-1 investment banks.

- Operational Inflection: In Q2 2026, SNEX delivered record-breaking fundamental acceleration, with total operating revenues climbing +64% Year-over-Year (YoY) to $1.6 billion, and net income surging +143% YoY to $174.3 million.

- Framework Return Verification: Backed by persistent macro volatility and cross-border structural flow growth, the core Arakawa Quant multi-factor strategy framework continues to achieve robust capital appreciation, tracking at +421.61% since inception in July 2022, compared to +96.50% for the S&P 500 benchmark.

- Asymmetric Valuation Corridor: Despite delivering a trailing one-year absolute return exceeding 119%, the asset maintains a severe multiple discount relative to the financial sector median, presenting a compelling valuation disconnect as consensus models materialize.

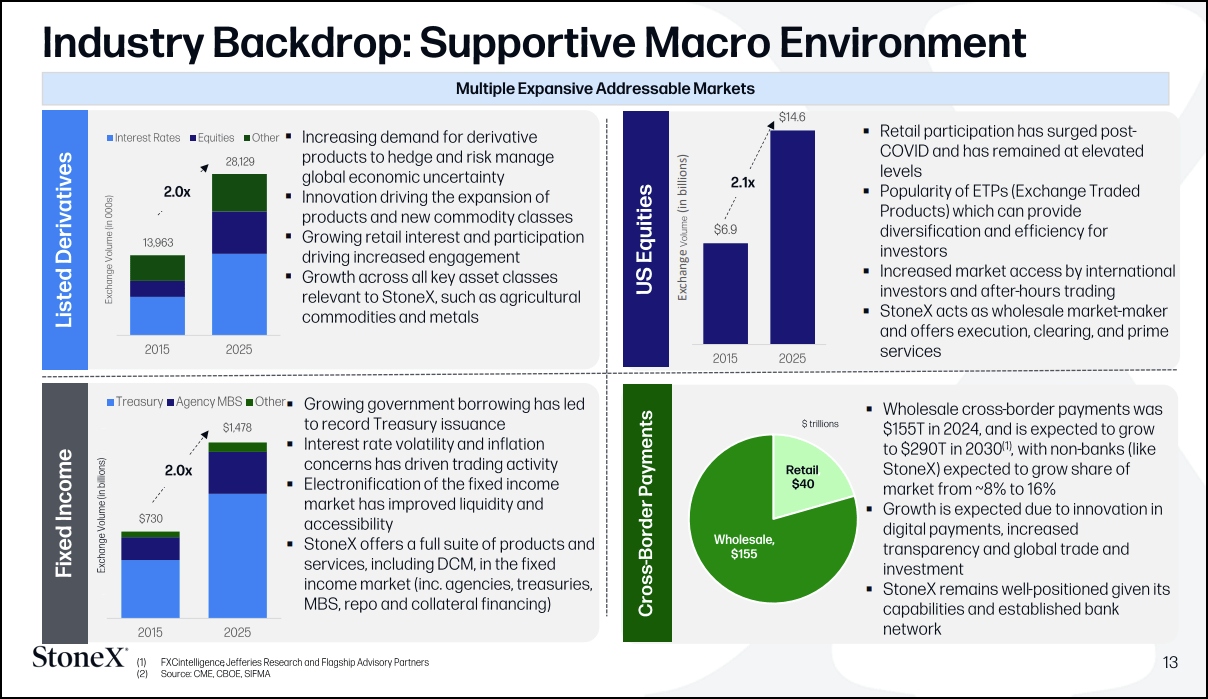

Macro & Business Architecture Analysis: The Non-Bank Flow Aggregator

Within the Arakawa Quant financial sector allocation engine, StoneX Group is structurally isolated not as a directional directional risk-taker, but as an indispensable transaction-flow and hedging utility. The firm's business model is explicitly engineered to extract recurring spreads, execution fees, and net interest income from real-economy volume flows across listed derivatives, OTC cleared contracts, physical commodities, and FX cross-border payments in over 140 currencies.

A core structural advantage is the sticky nature of its commercial client base—primarily agricultural producers, mining entities, and mid-sized enterprises utilizing customized OTC derivatives to manage physical price risk. This configuration builds high switching costs and creates counter-cyclical resilience: heightened market volatility and inflationary uncertainty directly stimulate corporate hedging velocity, lifting clearing fees and capital spreads simultaneously.

Furthermore, the post-merger integration of R.J. O’Brien has successfully solidified StoneX as the largest non-bank Futures Commission Merchant (FCM) in the United States, positioning the enterprise to capture up to $50 million in run-rate structural synergies.

Arakawa Quant Multi-Factor Matrix Alignment

The asset demonstrates an institutional grade profile across core growth and capital efficiency pillars, characterized by an under-followed analyst coverage base that yields significant pricing inefficiencies.

On a systematic factor basis, SNEX presents a premier combination of value and momentum. Q2 FY2026 performance underscores this momentum, with the Commercial operating segment expanding net operating revenues by 111%, fueled by a 98% jump in customized OTC structures and a 162% surge in physical contracts (predominantly precious metals). The Institutional segment concurrently scaled average daily securities volume past $12 billion.

Financially, net interest and fee income earned on expanding client float balances grew 54% to $154.5 million, providing a highly predictable baseline revenue anchor. With year-over-year and forward EPS growth metrics pacing 147% and 65% above the sector median respectively, the asset's valuation remain deeply depressed. Trading at an 84% discount on a trailing price-to-cash-flow basis relative to peer institutions, the equity is poised for structural re-rating, further supported by enhanced liquidity from its recent 3-for-2 stock split.

Systematic Risk Assessment and Defensive Boundaries

To enforce rigorous capital preservation, the quantitative framework establishes clear risk parameters:

- Counterparty Credit and Margin Volatility: As a central clearing intermediary, extreme market gaps can expose the firm to systemic margin-call defaults or collateral shortfalls if commercial clients experience localized hedging breakdowns.

- Cyclicality of Volume and Rates Regime: A macro transition toward low-volatility regimes or aggressive central bank rate cuts could compress both transaction-fee velocity and net interest margins on client float.

- Scale and Technology Competition: Sustaining market share against automated electronic brokerages and mega-banks requires continuous capital expenditure into internal clearing software and cybersecurity infrastructure.

Alpha is no longer found in raw data, but in the unseen structural correlations buried within institutional order flows.

Ada

Lead Quantitative Research Analyst

Subscribe to our newsletter

Get the insider insights you need to scale, straight to your inbox.

Decode the Market. Quantify Your Edge.

Elite quantitative models and real-time execution signals. Trade with institutional power.

Copyright © 2026 Hong Kong Arakawa Limited. All rights reserved.

%2C%20Color%3DNegative.svg)