搜索

AI Infrastructure Demand Surge: Sandisk (SNDK) Reports Q3 Revenue Up 251% Y/Y with Quarterly EPS Reaching $23.41

Core Summary

Systematic Compounding Validation: Since our quantitative strategy's inception in July 2022, the Quant Picks portfolio has continued to substantially outperform the broader market, returning +418% versus +100% for the S&P 500. Re-selecting SNDK into the core matrix validates the system's high win-rate criteria for high-growth structural transformations.

Infrastructure Hardware Placement: The company has successfully transcended its legacy consumer retail brand identity to cement itself as a core provider of high-performance storage for AI-driven cloud and data center environments, focusing on low-power, high-density SSDs that feed AI accelerators.

Business Model Evolution: The operational model has structurally shifted toward long-dated, financially backed supply agreements and firm volume commitments, drastically minimizing historical memory-cycle volatility and rewiring traditional industry risk profiles.

Macro Demand & Factor Realignment: Driven by premium customer mix, Q3 revenue skyrocketed 251% Y/Y to $5.95B with non-GAAP operating margins expanding to 70.9%. At a steep 93% discount on a forward PEG basis, backed by a new open-ended $6B buyback program, it provides a resilient vehicle for growth.

Macro & Architecture Assessment: Unifying Data Links Across Dense Compute Clusters

In the Arakawa Quant strategic research framework, the operational performance bottleneck of modern AI data centers has officially transitioned from standalone compute capacity to internal data transit velocity and raw power density limits. As parameters of generative large language models scale exponentially, linking thousands of distributed GPU nodes efficiently demands high-bandwidth, ultra-low latency physical storage layers.

In contemporary AI data center architectures, the GPU is no longer the sole determinant of computational yield. High-bandwidth, low-power storage architectures directly govern model training loops, inference latencies, and the ultimate return on infrastructure capital (ROI). SNDK leverages its deep intellectual property in flash cell design, advanced error-correction algorithms (ECC), and seamless controller-firmware integration to heavily depress power consumption relative to unoptimized legacy infrastructure. While it is not a frontline accelerator semiconductor vendor, its dense flash deployment stands directly in the critical path of AI compute, sustaining high data retrieval and continuous accelerator pipeline feeds.

SNDK: Core Beneficiary of the High-Performance Storage Ecosystem

As the artificial intelligence infrastructure landscape enters an extensive capital expenditure cycle, institutional focus within the semiconductor supply chain is pivoting. While the past few years prioritized absolute compute scale, the rapid expansion of hyperscale training clusters has exposed data retrieval and storage efficiencies as the defining variables of aggregate system performance. With data traffic across servers, switches, and clusters expanding exponentially, the network and storage layer is gaining massive structural weight.

High-Speed Enterprise Storage Architecture: Under this structural shift, the enterprise solid-state storage sector has emerged as a high-value niche within AI hardware. SNDK's core solutions—spanning proprietary flash controllers, optimized firmware, and dense solid-state enterprise arrays—serve as the critical traffic junctions inside high-throughput compute fabrics, ensuring accelerators are not starved of data during intense training iterations.

Efficiency and Bit-Power Margins: Data indicates that data-retrieval power overhead can bottleneck facility runtime in intense deep learning scenarios. Network and storage fabric efficiencies directly dictate total capital efficiency. SNDK's high-efficiency controller architectures maintain peak write/read execution while optimizing power per bit, a metric that has quickly become a primary baseline for hyperscaler procurement.

BiCS8 QLC "Stargate" Operational Execution: Furthermore, architectural standards are transitioning rapidly to next-generation high-density nodes. SNDK demonstrated elite operational discipline in Q3 FY26, intentionally holding bit shipments flat quarter-over-quarter to optimize inventory layout ahead of its BiCS8 QLC "Stargate" product release and the formal commencement of newly signed multiyear volume protections. This positions the company with high supply leverage and structural pricing power going into the second half of 2026.

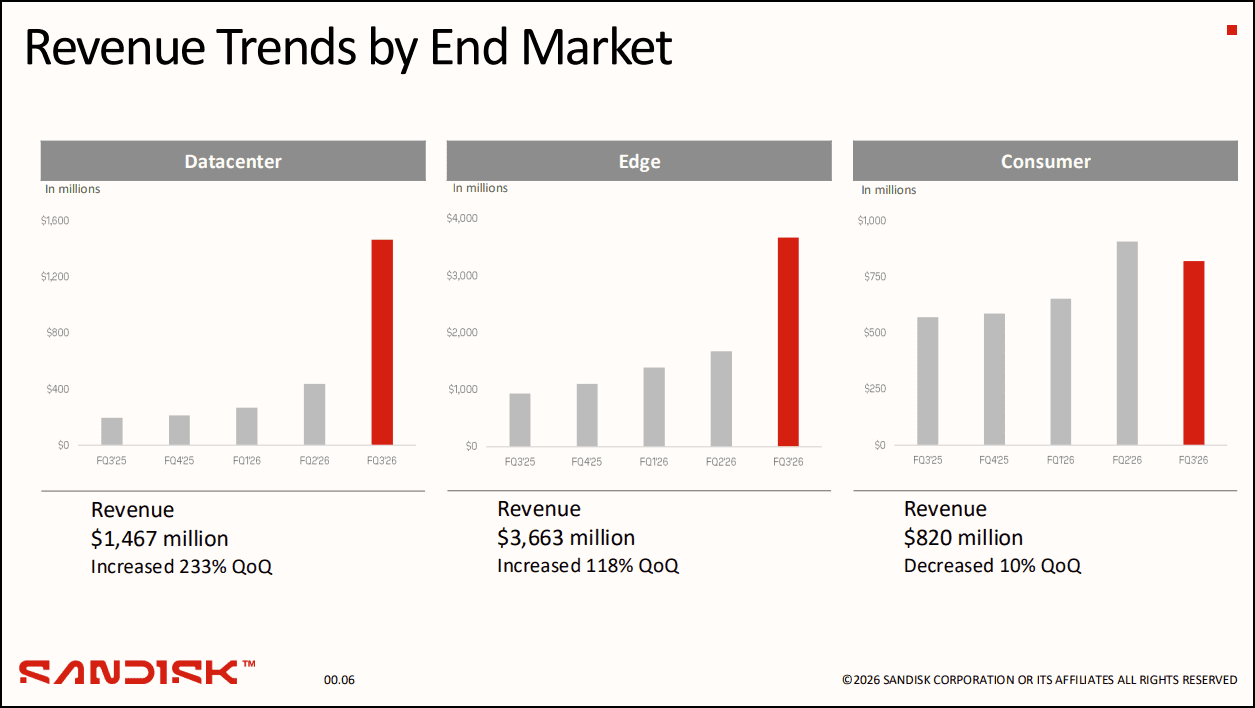

Source : SDNK Q3 2026 Investor Presentation

Arakawa Quant Multi-Factor Matrix and Factor Alignment

The asset displays a powerful confluence of Growth, Profitability, and Analyst Estimate Revision factors within our quantitative screening engine, yielding near-perfect metrics across fundamental clusters. The quantitative selection process completely strips away historical retail bias, relying solely on mathematical factor alignment.

From a purely quantitative financial stance, SNDK’s Q3 FY26 prints provided undeniable fundamental support:

Key Financial Performance Indicators | Prior Quarter Base | Q3 FY26 Actual Print | Y/Y Change |

|---|---|---|---|

Total Quarterly Revenue | $3.02B | $5.95B | +251% |

Data Center Segment Revenue | $0.44B | $1.47B | +233% (Q/Q) |

Edge Compute Segment Revenue | $1.68B | $3.66B | +118% (Q/Q) |

Blended Gross Margin | 51.1% | 78.4% | +2,730 bps |

Non-GAAP Operating Margin | 37.5% | 70.9% | +3,340 bps |

Diluted Earnings Per Share (EPS) | $6.2 | $23.41 | Beats $12-$14 Guidance |

With operating expenses scaled down to just 7.5% of top-line sales due to exceptional structural operating leverage, the core profitability indicators scaled exponentially. Adjusted free cash flow surged to $2.96B (representing approximately 50% of total revenue), pushing TTM cash per share to an exceptional $25.24 alongside a 39% return on equity (ROE). Long-term forward FWD EPS growth projections stand at 282%, vastly outpacing the tech hardware sector median of 17.53%.

While immediate price momentum looks extended on a standalone nominal basis—surging over 150% in the trailing three months—SNDK's forward Non-GAAP PEG ratio sits at a 93% discount to the sector average. This reveals that when normalized for its forward-looking secular growth velocity, the equity trades at a profound discount relative to peer multiples. Backed by a flawless upward revision matrix (14 positive EPS revisions, 13 positive revenue revisions, 0 downgrades over the past 90 days), the technical momentum is structurally anchored by real earnings power.

Systematic Risk Control and Boundary Auditing

To maintain institutional capital preservation guidelines, our quantitative frameworks enforce objective operational risk boundaries alongside upside capture:

Manufacturing Partner Concentration: SNDK maintains structural reliance on its joint production ventures with Kioxia (KXIAY). As a design- and system-focused enterprise, any unexpected alterations in corporate relationships, semiconductor foundry allocation, or shared engineering roadmaps represent an immediate upstream physical supply risk.

Contractual Execution Inflexibility: While long-dated supply agreements with firm volume guarantees mitigate traditional memory cyclicality, they naturally function as a double-edged sword. If hyperscaler workload parameters shift, alternative technological paths develop, or structural AI demand experiences an intermediate lull, these multiyear constraints could lock the company into rigid pricing structures, inducing costly renegotiation cycles.

Competitive Encroachment & Margin Reversion: The technological hardware supply chain remains exposed to cyclical down-cycles. SNDK continues to compete against larger, well-capitalized integrated device manufacturers capable of leveraging localized pricing wars. Additionally, whether a 78.4% gross margin represents a permanent structural plateau or an intermediate peak within an extended hardware build cycle remains subject to ongoing technical audit.

Conclusion

Sandisk (SNDK) has broken past its legacy consumer technology boundaries, positioning itself as a core beneficiary of the ongoing structural re-rating across the AI infrastructure storage layer. Its optimal matrix alignment across earnings revisions, price momentum, and deep forward PEG discounts underscores its fundamental competitive moat within hyperscale deployment. Complemented by a newly implemented, open-ended $6B stock buyback mandate, its medium-term trajectory presents a well-defined boundary for growth.