搜索

Global Market Weekly: AI Momentum Confronts Macro Stiffening and Rate Uncertainties

Market Summary

Macro Review: Global markets initiated the week in negative territory as institutional investors actively de-risked portfolios ahead of Nvidia’s highly anticipated earnings release.

Monetary Policy: Higher-than-expected inflation metrics have reignited anxieties surrounding a potential interest rate hike in the second half of 2026, compounding systemic market volatility.

Sector Performance: Despite early-week drawdowns, equities ultimately closed higher. Technology hardware led the broader market rally, while the Real Estate and Utilities sectors garnered strong support from defensive and income-oriented capital allocation.

Portfolio Strategy: In anticipation of multiple upcoming volatility catalysts, a barbell strategy—balancing high-growth assets with defensive, yield-generating equities—is recommended to fortify portfolio resilience.

Market Overview: AI Euphoria Intersects with Macro Hardening

U.S. equities faced downward pressure early in the week as market participants treated Nvidia’s (NVDA) fiscal earnings as a proxy referendum on the broader Artificial Intelligence (AI) secular trade. Ahead of the disclosure, systemic de-risking swept through megacap growth and AI-ecosystem names, mirroring patterns observed in previous earnings cycles.

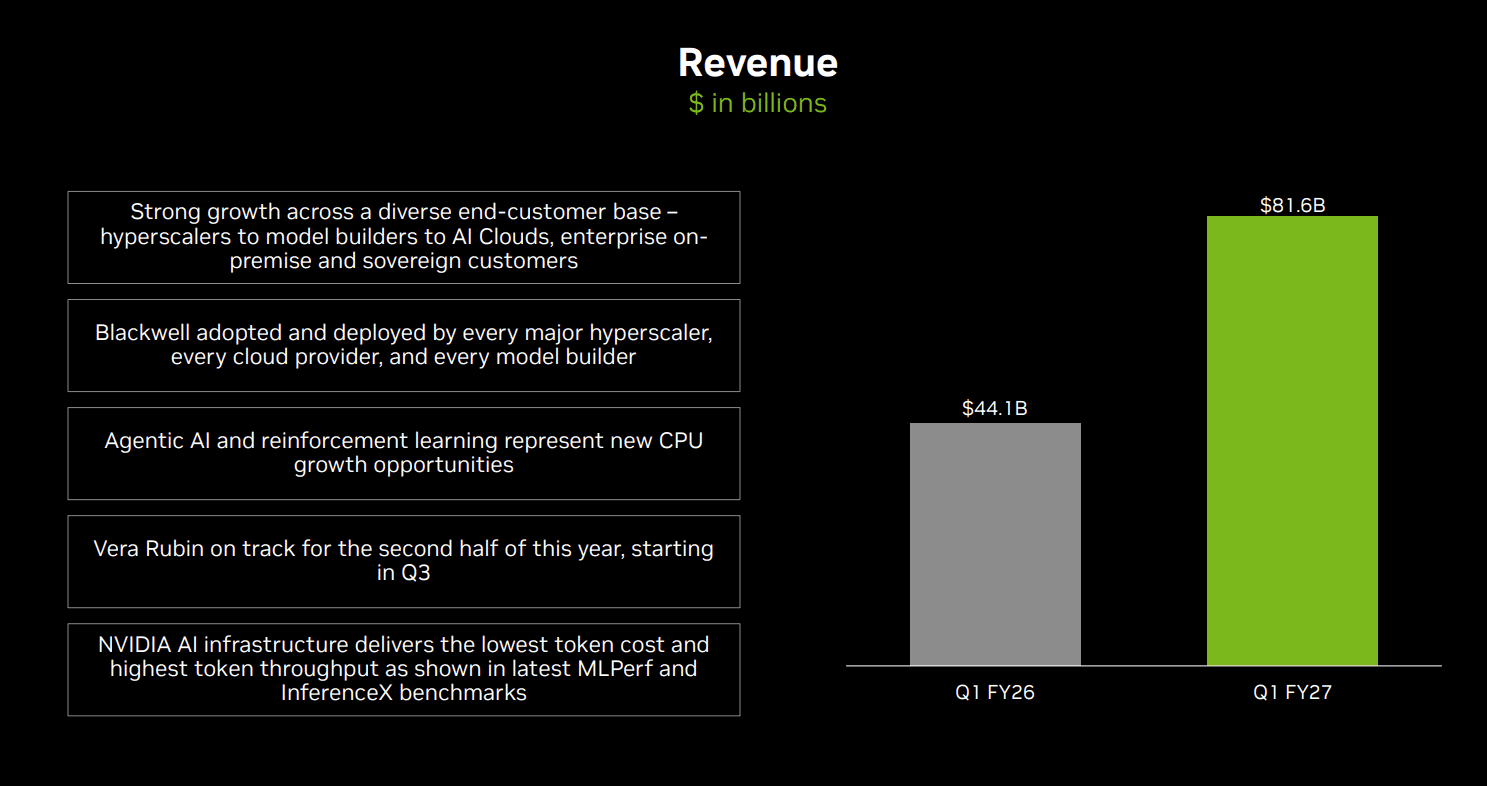

Despite heightened pre-earnings anxiety, Nvidia delivered stellar quarterly results, sustaining its exponential top-line expansion (+85% Y/Y) alongside robust operating margins. However, subsequent profit-taking reflected broader market concerns that peak near-term growth had already been priced in, even as the fundamental prints reaffirmed the long-term AI structural bull case.

Q1 FY27 Nvidia Investor Presentation

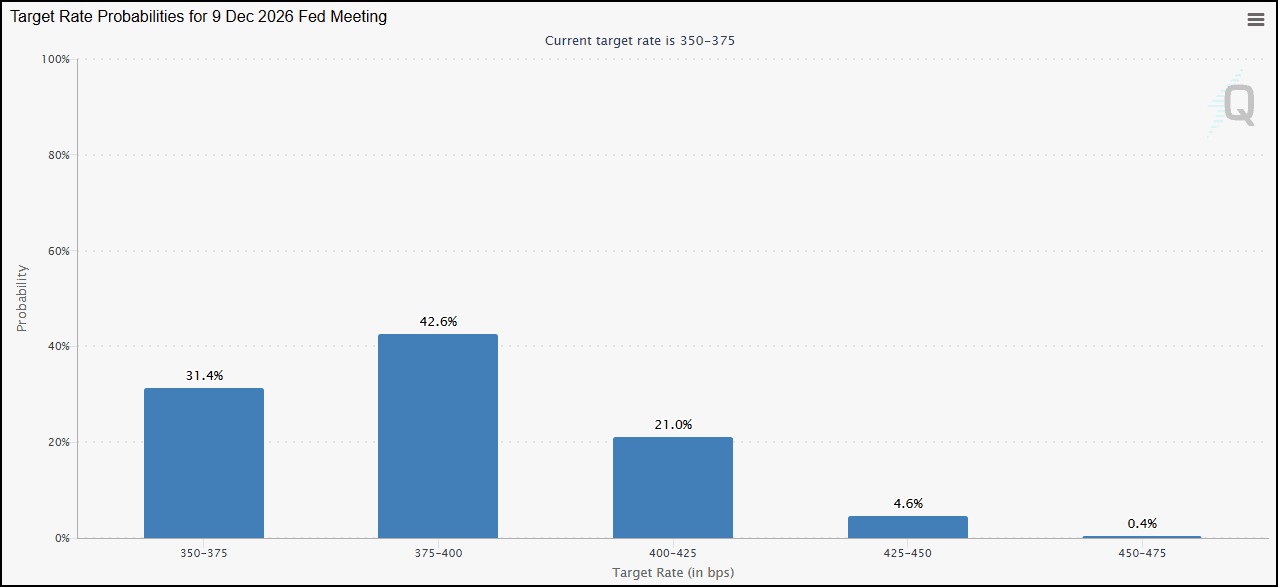

Simultaneously, early-week volatility was exacerbated by persistent macroeconomic headwinds following hotter-than-expected CPI and PPI data. The ensuing fixed-income selloff pushed long-dated Treasury yields higher and triggered a hawkish repricing of monetary policy. CME FedWatch data indicates an approximate 70% implied probability that the Federal Reserve will lift interest rates above the current target range in H2 2026.

CME FedWatch

This policy uncertainty is further amplified as newly sworn-in Fed Chair Kevin Warsh inherits a deeply fragmented Federal Open Market Committee (FOMC). This internal division was recently underscored by Governor Christopher Waller’s remarks, which indicated that further monetary tightening cannot be ruled out if inflationary pressures fail to decelerate toward target levels.

Despite these overlapping macroeconomic and geopolitical crosscurrents, major benchmarks—including the Dow Jones Industrial Average, S&P 500, and Nasdaq Composite—staged a late-week recovery. A sharp rebound in technology hardware stocks successfully offset the headwinds of restrictive Fed commentary and escalating yields. Additionally, improving geopolitical sentiment regarding potential diplomatic breakthroughs in the Iran conflict stabilized energy markets, reversing the losses previously triggered by spiking crude prices.

On a trailing one-month basis, while the Technology sector (XLK) consolidated some of its historical gains, capital rotated into Real Estate (XLRE), sustained by resilient structural housing demand and asset-backed equity allocations. Concurrently, Utilities (XLU) experienced strong inflows as institutional investors sought low-beta, high-dividend defensive sectors to insulate portfolios against lingering macroeconomic ambiguity.

Quantitative Strategy and Portfolio

In highly volatile environments, utilizing a systematic, multi-factor quantitative framework eliminates behavioral bias from asset allocation. By strictly screening equities across five core pillars—Valuation, Growth, Profitability, Momentum, and Earnings Revisions—investors can effectively isolate fundamentally superior companies positioned to generate persistent alpha.

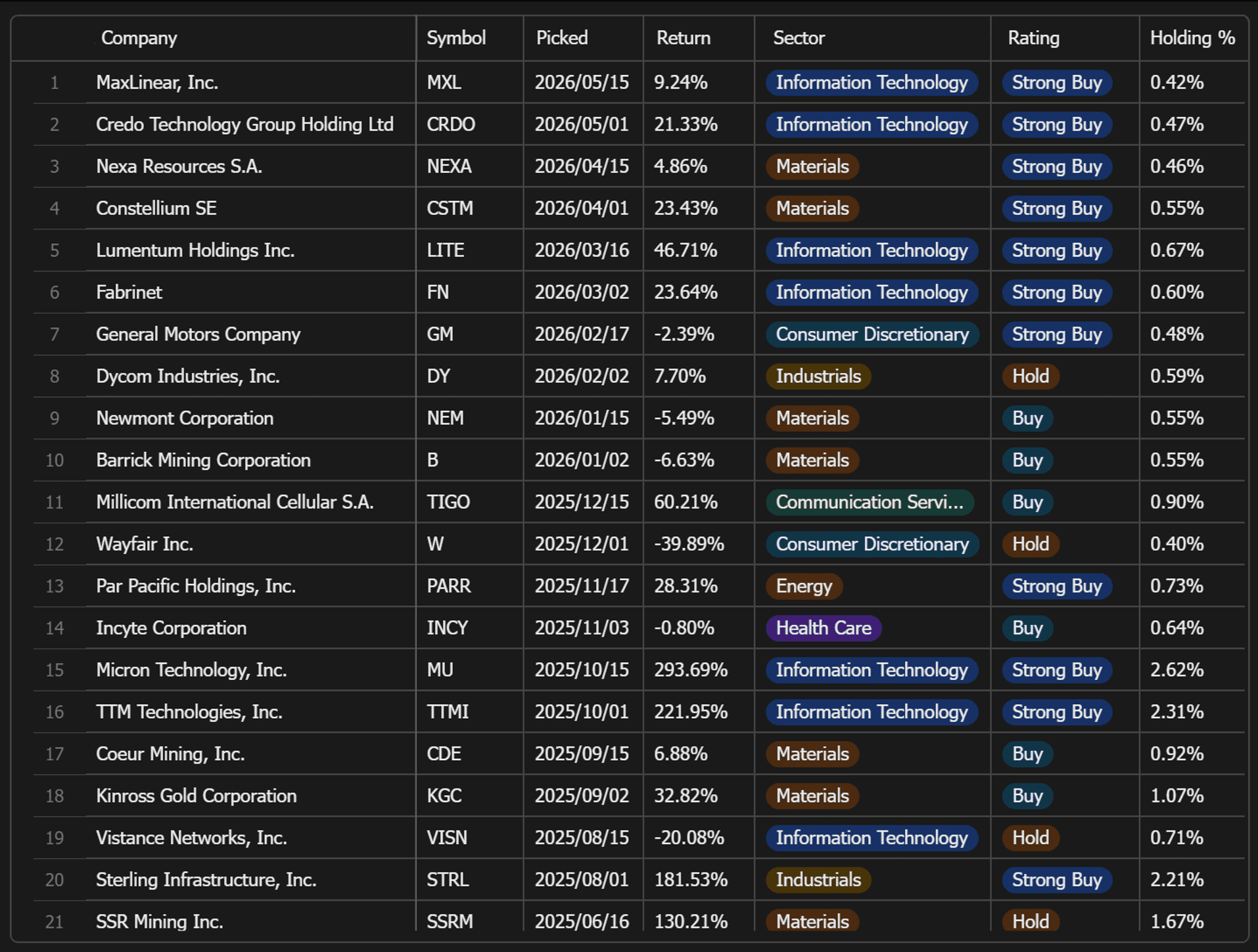

During the recent market swing, high-growth data center infrastructure enablers led the recovery as capital rotated back into the AI value chain. For instance, MaxLinear (MXL) experienced sharp upward momentum due to its strategic positioning within the accelerator build-out.

In the enterprise software space, Okta (OKTA) rallied following several institutional upgrades citing accelerating demand for identity-access management architecture. Conversely, in the consumer sector, Wayfair (W) advanced as sustained cost-rationalization and margin-expansion initiatives validated its corporate turnaround thesis.

High-Performing and Underperforming Equities (Weekly Review)

Top Contributors: Technology enablers and infrastructure platforms led short-term performance as secular growth trends reasserted dominance post-earnings.

Laggards and De-risking: Sterling Infrastructure (STRL) surrendered a portion of its post-earnings gains as institutional investors locked in profits following an extended parabolic run. Blue Bird (BLBD) similarly consolidated post-rally. In the commodities space, SSR Mining (SSRM) and other precious metals names faced headwinds from rising real yields and a rotation into risk-on assets.

Institutional Strategy: Deploying the Arakawa Quant Barbell Allocation

We are operating within an anomalous macroeconomic regime: despite sticky inflation prints, cloudier forward visibility, and elevated intraday volatility, broad equity benchmarks like the S&P 500 continue to challenge historical highs amid structural dispersion.

Portfolio Construction Insight: To navigate these complex crosscurrents, executing a disciplined barbell strategy is paramount. By blending high-beta, secular growth names with low-beta, high-yield defensive equites, a portfolio can successfully capture structural upside beta while maintaining robust downside drawdown protection.

A premier quantitative growth strategy must not only outperform traditional benchmarks on capital appreciation but must also demonstrate superior cash-flow generation capability. Currently, the multi-factor equity portfolio screened by the Arakawa Quant engine delivers an average forward dividend yield of 1.47%, establishing a statistically significant yield premium over the S&P 500’s average yield of 0.97%.

To institutionalize this systematic asset allocation, institutional investment committees are increasingly integrating the advanced Arakawa Quant architecture. This mathematical model precisely optimizes factor exposures across yield sustainability, growth durability, and balance sheet safety. By implementing an equal-weighted matrix and a weekly systematic rebalancing mandate across liquid U.S. equities and ADRs, the Arakawa Quant framework extracts persistent alpha backed by empirical data, isolating institutional portfolios from behavioral biases and market sentiment shocks.