搜索

Institutional Capital Review: High Yields and Crude Compounding Market Breadth Compression

Executive Summary

Macro Headwinds: Hotter-than-expected inflation metrics paired with WTI crude breaking above $100/bbl have intensified concerns of a prolonged restrictive monetary policy regime under intensifying geopolitical strains.

Fixed Income Selloff: Sovereign debt markets experienced significant capital outflows, driving the benchmark 10-Year U.S. Treasury yield to a one-year high of 4.60%.

Market Breadth: While the Technology factor sustained its rolling monthly outperformance, market breadth collapsed significantly toward the end of the trading week, leaving Energy as the sole positive sector during the Friday session.

Key Catalysts: Asset allocators are tracking the structural outcome of the U.S.–China summit, developments along the Strait of Hormuz, and hyperscaler capital expenditure trends ahead of major semiconductor earnings disclosures.

Macro Review: Stagflationary Signals and Fixed-Income Re-Pricing

Global equity benchmarks struggled for direction as market participants digested hotter-than-expected CPI and PPI prints alongside a persistent structural squeeze in energy markets. With crude oil holding firmly above $100 per barrel—driven by disruptions around the Strait of Hormuz and broader Middle Eastern conflicts—supply-side inflation pressures have materially hardened.

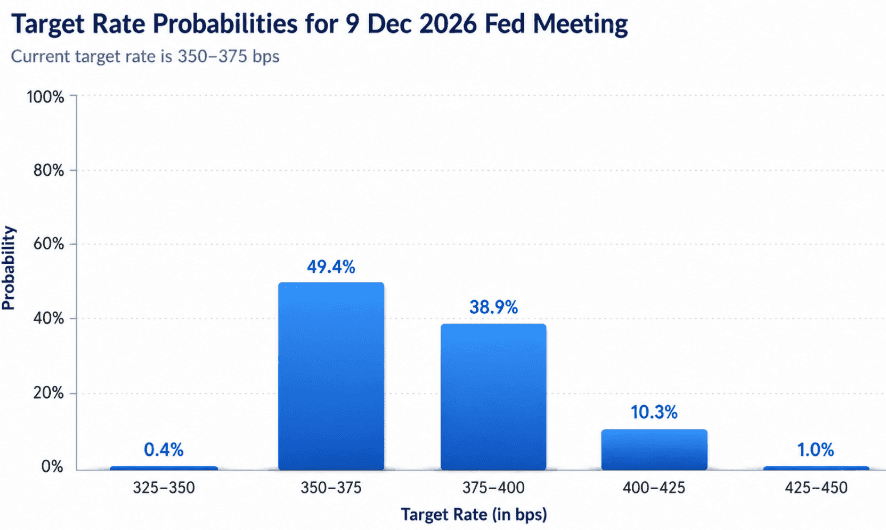

FedWatch Tool, CME Group, as of 12:00 pm, May 15, 2026

This inflationary backdrop triggered a severe selloff across the fixed-income curve, thrusting the 10-Year U.S. Treasury yield ($$US10$$) to 4.60%, its highest level in 12 months. The rapid steepening of the yield curve has tightened financial conditions, altering equity discount rates and compressing equity risk premiums. CME FedWatch pricing reflects a dramatic hawkish pivot, indicating an implied probability of approximately 50% that the Federal Reserve will implement an additional interest rate hike within the calendar year, a challenging backdrop for newly appointed Fed Chair Kevin Warsh.

Concurrently, the highly anticipated U.S.–China summit yielded a constructive diplomatic tone but lacked tangible structural concessions regarding trade frameworks, semiconductor supply chains, or technology policy cooperation. Growth equities faced late-week headwinds as institutional desks noted the lack of definitive progress on bilateral chip-trade agreements, causing capital to rotate out of high-duration growth factors under pressure from escalating discount rates.

Industry Allocation and Sector Dispersion Analysis

While broad indexes remained range-bound, underlying market breadth metrics deteriorated significantly. This dispersion is illustrated by the divergence between secular growth themes and cyclical energy plays, contrasted against interest-rate-sensitive defensive factors.

The primary risk factor under observation is the narrowing of market breadth. Over the past month, mega-cap technology and semiconductor components accounted for the vast majority of index gains, driven by persistent hyperscaler AI data center build-outs. However, by the final session of the week, this concentration risk became evident as Energy emerged as the only positive sector, highlighting the vulnerability of the broader market to factor crowding.

Arakawa Quant Factor Evaluation and Alpha Generation

In a macroeconomic regime characterized by rising cost-of-capital and supply-side constraints, deploying a disciplined, data-driven framework like the Arakawa Quant engine eliminates behavioral biases from asset allocation. By systematically screening the investable universe across five fundamental pillars—Valuation, Growth, Profitability, Momentum, and Earnings Estimate Revisions—the Arakawa Quant model isolates structural alpha while mitigating systematic downside risk.

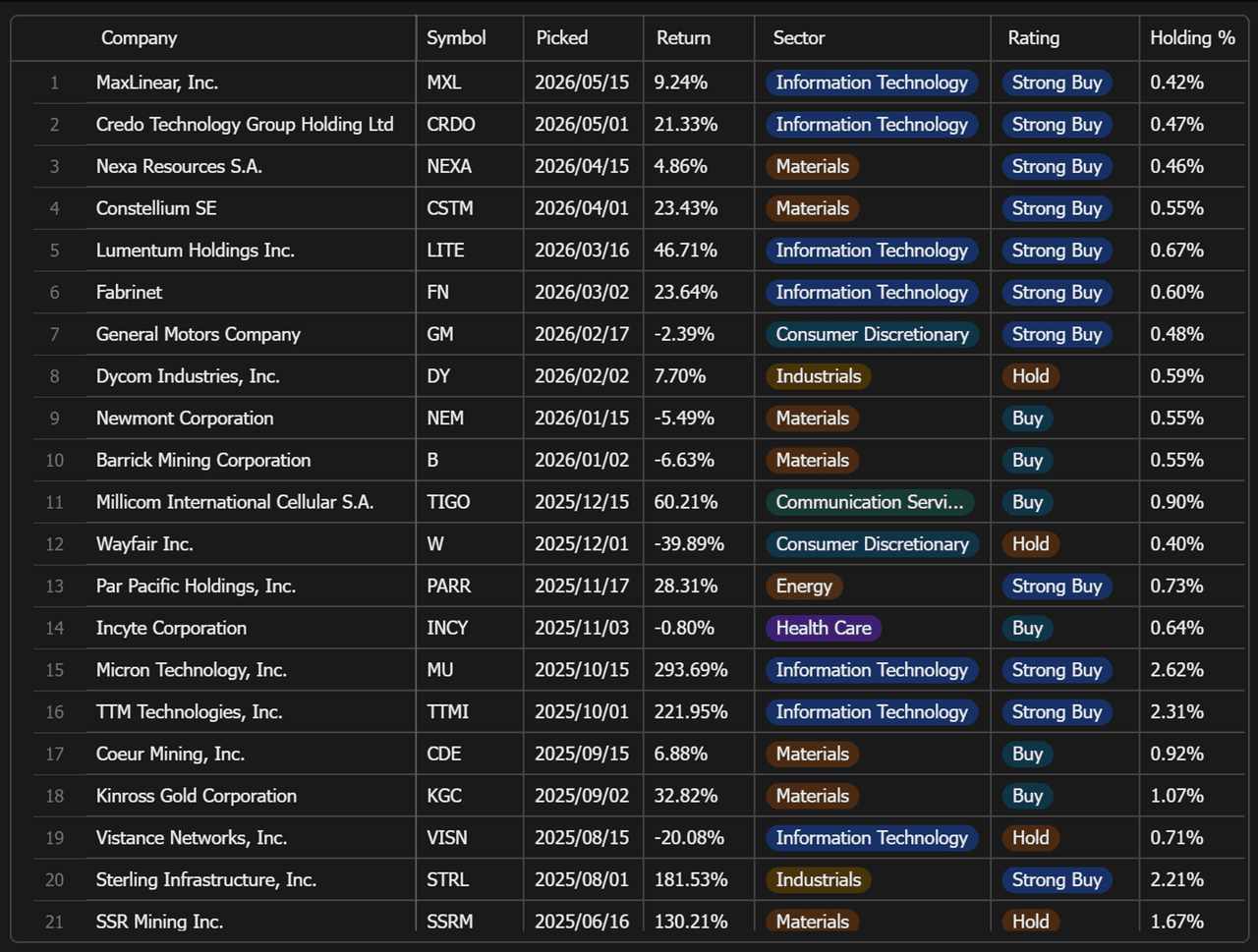

Quantitative Outliers: Weekly Drivers

During the recent rotation, specific sub-industries exhibited distinct factor profiles:

Advanced Hardware and AI Infrastructure: Semiconductor and optical networking enablers continued to attract heavy institutional inflows. Micron Technology (MU) rallied due to escalating demand visibility for high-bandwidth memory (HBM) architectures. Fabrinet (FN) and Lumentum Holdings (LITE) gained on accelerating datacom and optical connectivity infrastructure spend, while TTM Technologies (TTMI) advanced due to resilient defense and aerospace electronics demand.

Industrial Electrification Secular Tailwinds: Nexa Resources (NEXA) broke out to the upside, supported by global copper and zinc supply deficits alongside long-term infrastructure and grid-modernization demand.

Consumer Discretionary and Capital Drag: Conversely, travel and leisure operators such as Carnival Corporation (CCL) and Royal Caribbean Cruises (RCL) faced compression as rising crude prices threatened operating margins via fuel inputs, alongside concerns of declining consumer discretionary wallets. Brinker International (EAT) underperformed due to wage and food margin compression, while Wayfair (W) collapsed under the weight of higher mortgage and borrowing costs. Financial anchors like Manulife Financial (MFC) retrenched as bond market volatility destabilized long-term insurance asset liability matching models.

Institutional Strategy: Quantitative Risk Management

Navigating this landscape requires shifting away from passive indexing into rules-based, systematically rebalanced models. Advanced multi-factor models optimized for yield durability, fundamental safety, and growth persistence offer a superior defensive shell compared to traditional dividend ETFs.

By applying an equal-weighted, systematically adjusted framework across liquid equities and ADRs, asset managers can capture structural themes—such as the AI hardware build-out and localized energy insulation—while eliminating individual stock concentration risk and protecting capital against monetary policy surprises.