搜索

Navigating Pre-Earnings Valuation Resets: Constructing a Quantitative Barbell Midst Tech Volatility

Executive Summary

Market Sentiment: Risk asset valuations compressed following a hotter-than-expected inflation print, coupled with broad portfolio de-risking ahead of Nvidia’s crucial fiscal earnings release.

Infrastructure Reset: High-flying Artificial Intelligence (AI) infrastructure equities experienced a targeted technical selloff as institutional managers locked in profits and normalized factor exposures.

Historical Context: Long-term capital allocators view this drawdown as a standard mid-cycle corrective phase, drawing structural parallels to Celestica’s $$\si$$30% retrenchment in Q1 2025 prior to its subsequent multi-hundred percent alpha generation.

Portfolio Architecture: To mitigate overlapping geopolitical, political, and monetary volatility catalysts, a disciplined barbell framework—allocating between secular growth and low-beta, high-yield defensive equities—remains paramount.

Macro Dynamics: Inflation Pressures and Pre-Earnings Anxiety

Global equity markets exhibited pronounced intraday volatility as market participants treated the upcoming Nvidia (NVDA) quarterly earnings disclosure as an implied referendum on the secular AI theme. This setup mirrors previous cyclical inflections, notably November 2025, where blockbuster fundamental prints triggered short-term "sell-the-news" profit-taking before long-term institutional accumulation drove the asset to its current $$+18\$$ year-to-date (YTD) performance.

This specific consolidation phase is further complicated by persistent macroeconomic headwinds. Sticky core inflation has pushed the long end of the U.S. Treasury curve higher, prompting fixed-income and equity desks to reprice a "higher-for-longer" monetary policy regime. This expansion in the risk-free rate ($$R_$$) naturally compresses equity risk premiums (ERP), disproportionately impacting high-duration growth sectors, with Technology emerging as the primary underperformer during this capital rotation.

Case Study in Market Resiliency: Distinguishing Correction from Capitulation

While the sudden drawdown across the AI infrastructure ecosystem may appear unsettling, empirical data suggests this represents a healthy, non-systemic valuation reset rather than a structural breakdown.

A prominent historical analog is Celestica (CLS). In Q1 2025, amidst intense macroeconomic and geopolitical ambiguity surrounding the U.S. presidential transition, tariff implementation risks, and shifting fiscal policy projections, CLS suffered a peak-to-trough retracement exceeding 30%. This selloff intensified through early Q2 2025 following major administration policy announcements. However, because the underlying corporate fundamentals remained intact, the equity ultimately bottomed and subsequently generated a $$+330\$$ return from its cyclical lows.

Long-term performance analytics back this quantitative methodology. Historical data spanning over 15 years tracking top-tier, fundamentally screened quantitative equities demonstrates that executing an accumulation strategy during market drawdowns of $$15\$$ or greater yields significant asymmetric upside. On average, buying top-factor-rated equities during these corrective phases generated a two-year forward return of 117%, outperforming the broader S&P 500 benchmark by more than 2x over the identical investment horizon.

Portfolio Architecture: The Arakawa Quant-Driven Barbell Model

As macro visibility remains clouded by sticky core inflation, localized sector shocks, and the upcoming November midterm elections, maintaining an unhedged, single-direction long portfolio exposes institutional capital to excessive systematic beta risk.

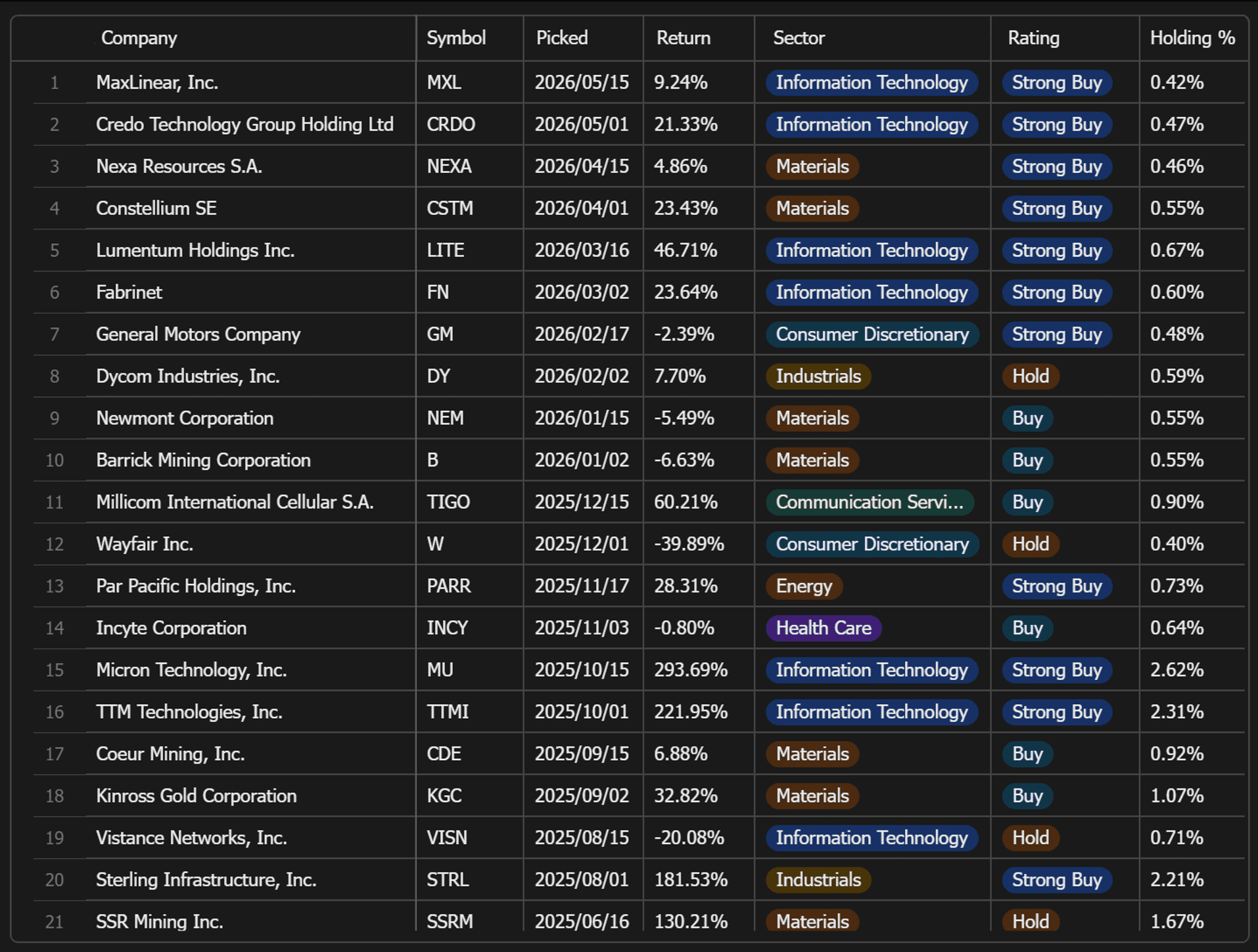

Implementing a strict Arakawa Quant barbell framework allows asset allocators to capture structural growth themes while insulating equity capital via robust cash-flow generation. Within this cross-factor architecture, the growth sleeve optimizes total return and capital appreciation, while the defensive sleeve leverages high-conviction dividend equities screened through the Arakawa Quant proprietary safety matrix.

Currently, the growth-and-income portfolio optimized by the Arakawa Quant multi-factor model maintains an average forward dividend yield of 1.50%, establishing a superior yield spread over the S&P 500's average yield of 0.97%.

To institutionalize this systematic strategy, the Arakawa Quant engine executes a rules-based, three-tiered operational framework:

Sovereign Universe Filtration: Dynamically filtering an institutional pool of nearly 5,000 highly liquid U.S. equities and ADRs.

Dividend Quality Stratification: Utilizing Arakawa Quant metrics to perform deep-dive audits on dividend compound growth rates, free cash flow (FCF) payout sustainability, and balance sheet resilience. Historical backtesting indicates that restricting allocations to the top 20% of equities within the Arakawa Quant Dividend Safety spectrum successfully insulated portfolios from 98% to 99% of realized corporate dividend reductions.

Equal-Weighted Systematic Rebalancing: Deploying disciplined, weekly systematic rebalancing across the portfolio. This mitigates single-stock concentration risks and exploits intra-week volatility to harvest systematic algorithmic gains through mathematical mean reversion.