搜索

Base Metals Matrix: Nexa Resources (NEXA) Captures Zinc Supply Deficits via Integrated Mine-to-Smelter Model

Executive Summary

Systematic Rebalancing: Nexa Resources S.A. (NEXA) has entered the active quantitative selection matrix, driven by a highly favorable 2026 zinc macro regime characterized by structural inventory depletion, resilient industrial demand, and sticky pricing corridors.

Structural Edge: The issuer operates a rare, highly optimized integrated mining and smelting architecture. This structural pairing stabilizes corporate operating margins across complex commodity down-cycles and mitigates merchant concentrate pricing volatility.

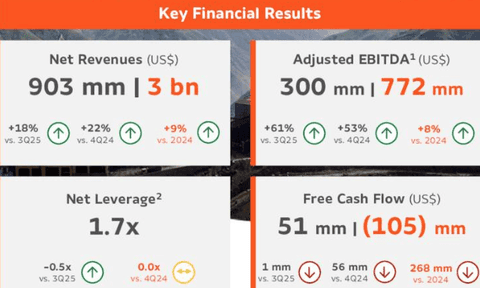

Financial Acceleration: Historical Q4 disclosures confirmed an operational inflection, with consolidated net revenues scaling +22% Year-over-Year (YoY) and adjusted EBITDA surging +53% YoY, driven by a combination of elevated London Metal Exchange (LME) spot cash pricing and unit-level operational efficiencies.

Polymetallic Hedging: While zinc remains the core economic driver, NEXA's secondary revenue vectors in copper, lead, silver, and gold provide an organic multi-asset cushion against single-commodity downside.

Macro & Commodity Regime Analysis: Exploiting Structural Zinc Deficits

Nexa Resources Quarterly Earnings Presentation

Within the Arakawa Quant commodity allocation framework, zinc has transitioned into an aggressive structural expansion phase in the 2026 fiscal year. Global LME and Shanghai exchange warehouse inventories have contracted to critical baseline parameters, driven by systemic mining supply disruptions and smelting capacity curtailments across traditional jurisdictions. NEXA captures this macro tailwind directly through its extensive asset footprint in Latin America.

The core operational differentiator for NEXA is its vertically integrated architecture. Unlike pure-play mining operators exposed to shifting Treatment Charges (TCs) or independent smelters vulnerable to raw material scarcity, NEXA processes its own mined concentrate internally. This loop insulates corporate cash flows from supply-chain friction and maximizes margin capture per metric ton of refined metal.

Furthermore, strategic long-life initiatives—specifically the optimization of the Aripuanã project and the technical integration of the Cerro Pasco infrastructure—are systematically extending overall mine life while shifting the net asset value (NAV) curve upward.

Arakawa Quant Multi-Factor Matrix Alignment

Valuation Mispricing

The asset presents a profound valuation disconnect, trading at deep discounts to global basic materials benchmarks despite outpaced forward EBITDA acceleration and an absolute lack of downward sell-side revisions.

From a quantitative factor perspective, NEXA represents a classic value-growth anomaly within cyclical industries. The company’s Forward P/E of 4.26x represents a 73% discount to the global materials sector median, while its Forward EV/EBITDA of 2.59x reflects a 69% discount.

This extreme multiple compression occurs precisely as the issuer’s forward EBITDA growth tracking parameter (12.31) exceeds the sector median by 49%. Driven by robust by-product silver and gold cash credits, the asset's underlying cash-generation capability is systematically mispriced by passive indices.

The institutional thesis is further validated by trailing 90-day consensus revision behavior: 2 EPS models and 3 top-line revenue models have been updated exclusively upward, capturing the commodity price action without experiencing localized downgrade flows.

Cash Flow Quality

Market pricing of NEXA continues to be anchored in a narrow zinc-centric framework, overlooking the stabilizing effect of its diversified by-product revenue structure.

As a leading base metals producer in Latin America, the company generates additional revenue streams from silver, gold, copper, and lead. In a macro environment characterized by resilient precious metal pricing and gradual industrial demand recovery, this multi-commodity exposure materially reduces earnings volatility at the consolidated level.

From a free cash flow perspective, by-product contributions partially offset mining and processing costs, enhancing downside resilience during cyclical downturns while preserving upside convexity during commodity upswings. This hybrid profile of cyclicality and cash flow stability is structurally uncommon within the global materials universe.

Earnings Revisions and Operational Re-rating

Over the past 90 days, sell-side analysts have delivered a consistent upward revision pattern, including two EPS upgrades and three revenue forecast increases, without any negative revisions. This level of directional consistency is atypical for commodity-linked equities given inherent price volatility.

From a quantitative perspective, the simultaneous presence of low valuation, positive earnings revisions, and improving cash flow metrics typically corresponds to an early-stage repricing phase within cyclical bull cycles. NEXA’s current factor configuration closely resembles historical inflection periods in base metals markets.

Importantly, the upward revisions are not solely driven by commodity price assumptions, but also reflect improvements in operational efficiency and capacity realization. This reduces the company’s marginal dependency on external price fluctuations and increases the structural visibility of earnings growth.

Multi-Factor Convergence Signal

From an Arakawa Quant scoring perspective, NEXA does not exhibit strength in a single dimension alone, but rather demonstrates simultaneous reinforcement across multiple factors, including:

Value Factor

Earnings Revision Factor

Cash Flow Quality Factor

Commodity Cycle Momentum Factor

Historically, such synchronized factor reinforcement has coincided with regime shifts in market valuation. NEXA currently resides in a zone where deep valuation discounts coexist with improving fundamentals and upward earnings momentum, indicating a persistent gap between market pricing and intrinsic value formation.

Systematic Risk Assessment and Defensive Boundaries

To insulate institutional deployments against systemic commodity drawdowns, the quantitative framework establishes strict risk parameters:

Commodity Spot Sensitivity: Despite polymetallic diversification, NEXA’s rolling cash flow generation remains highly sensitive to LME zinc pricing. A sudden macroeconomic deceleration or a strengthening U.S. Dollar Index ($$DX$$) could compress spot margins.

Operational Execution Complexities: Multi-asset mining complexes are inherently exposed to localized cost inflation, geological extraction constraints, and ramp-up bottlenecks at newer facilities like Aripuanã.

Jurisdictional and Regulatory Overlays: Operating heavily within South American mining jurisdictions introduces localized environmental compliance cost structures and shifting fiscal policy parameters that mandate persistent governance monitoring.

Conclusion

NEXA is fundamentally a structural beneficiary of the global zinc supply contraction cycle rather than a pure cyclical miner. Its vertically integrated model and diversified by-product exposure enhance both cash flow stability and cyclical upside. Within the Arakawa Quant framework, the convergence of low valuation, improving earnings revisions, and an upturn in the commodity cycle signals a multi-factor re-rating process. Overall, the market still appears to underappreciate its ongoing fundamental improvement, suggesting the revaluation phase is still in its early stages.