搜索

Semiconductor Architecture Layer: MaxLinear (MXL) Positions as Critical AI Optical Interconnect Enabler Amid Exponential Data Center Capex

Executive Summary

Strategic Positioning: MaxLinear, Inc. (MXL) operates as a critical fabless enabler deeper in the AI infrastructure stack, specializing in highly integrated mixed-signal, RF, and analog Systems-on-Chip (SoCs) that facilitate ultra-high-speed data transmission between GPUs, switches, and clusters.

Financial Acceleration: In Q1 2026, MXL delivered a powerful operational pivot, with revenue surging +43% Year-over-Year (YoY) to $137 million, alongside significant upward adjustments to forward optical data center revenue guidance.

Systematic Portfolio Performance: Despite mid-year macroeconomic volatility, the Arakawa Quant multi-factor core framework continues to demonstrate significant resilience, generating a cumulative total return of +398% since initialization in July 2022, compared to +98% for the S&P 500 benchmark.

Unanimous Revision Vector: Driven by extensive design wins with premier cloud service providers across the U.S. and Asia, institutional sell-side analysts have executed unanimous upward revisions, positioning the asset for sustained operating leverage.

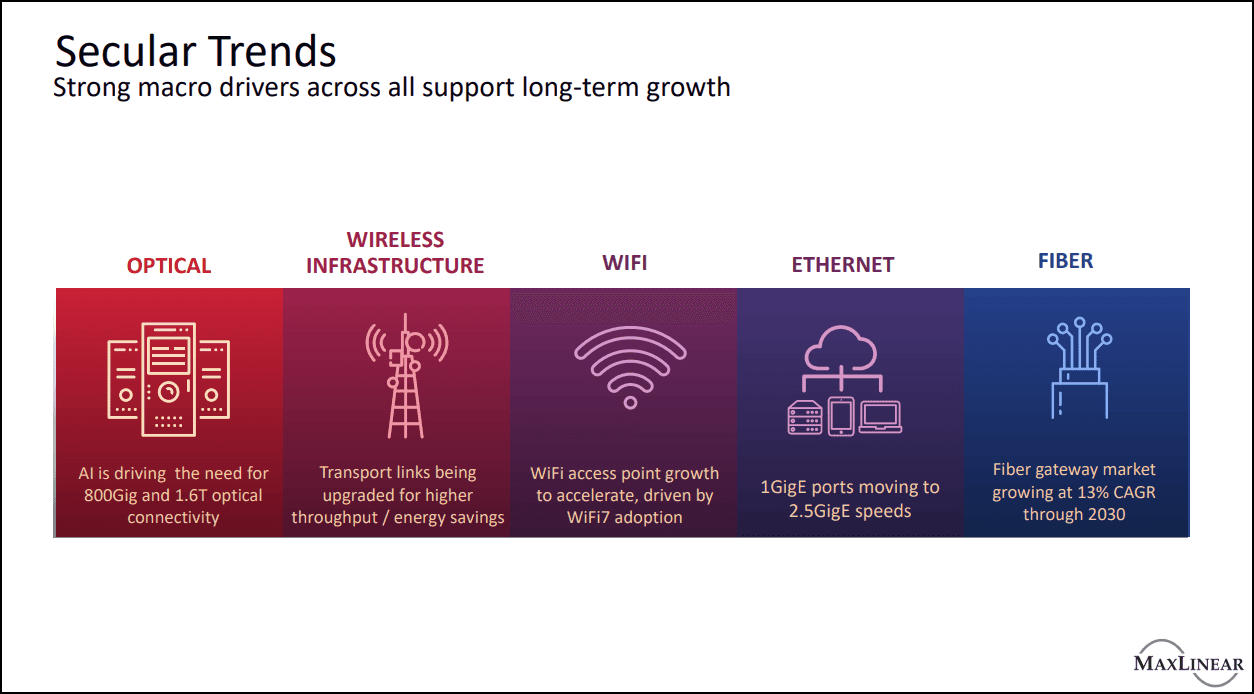

AI Infrastructure Expansion Is Driving a Revaluation of the Connectivity Layer

Nexa Resources Quarterly Earnings Presentation

As hyperscale cloud providers continue to accelerate investments in artificial intelligence infrastructure, market attention has largely focused on GPUs, AI accelerators, and cloud computing platforms. However, as training clusters scale from thousands to tens of thousands of GPUs, the primary bottleneck to overall computing efficiency is no longer raw computational power alone—it is the speed and reliability of data transmission across servers, switches, storage systems, and AI accelerators.

For large language models (LLMs), every training and inference workload requires massive volumes of data to move seamlessly across distributed computing environments. As cluster sizes expand, traditional copper-based architectures increasingly suffer from signal degradation, higher latency, and rising power consumption. Consequently, the investment thesis surrounding AI infrastructure is evolving from a pure “compute-layer competition” toward a broader “connectivity-layer competition.”

At the same time, data center network architectures are rapidly migrating toward 800G and eventually 1.6T optical interconnect standards. High-speed signal processing and optical networking infrastructure are becoming mission-critical components of next-generation AI deployments. For hyperscale AI clusters, network throughput has emerged as one of the most important determinants of overall system efficiency, positioning connectivity solutions as a key beneficiary of the current data center capital expenditure cycle.

MaxLinear: A Critical Connectivity Layer Asset Within the AI Ecosystem

Arakawa Quant classifies MaxLinear (NASDAQ: MXL) as:

“Not a frontline GPU supplier, but a critical connectivity-layer asset within AI infrastructure.”

Unlike GPU manufacturers that directly participate in computational workloads, MaxLinear provides the mixed-signal connectivity solutions that enable high-speed data transmission throughout AI clusters. Its products are widely deployed in optical modules, active optical cables (AOCs), switch interconnects, and data center networking architectures, making them essential components of modern AI infrastructure.

Unlike many traditional semiconductor companies, MaxLinear operates under a fabless business model, allocating capital toward chip architecture development and product innovation rather than manufacturing assets. This asset-light approach not only enhances return on invested capital (ROIC) but also provides management with greater flexibility to adapt to rapidly evolving data center networking requirements.

Through years of engineering investment, the company has successfully integrated signal reception, digital signal processing (DSP), power management, and hardware-level security functions into highly integrated SoC solutions. This architecture improves deployment efficiency, lowers system complexity, and increases overall customer value.

More importantly, MaxLinear’s growth narrative has fundamentally changed.

Historically viewed primarily as a broadband and RF connectivity supplier, the company is increasingly transitioning toward higher-growth and higher-margin markets, including data center optical interconnects, 5G backhaul infrastructure, and enterprise-grade Wi-Fi 7 networking solutions.

This strategic transformation not only expands the company’s addressable market but also improves its revenue quality, margin profile, and customer mix.

From an industry positioning perspective, MaxLinear's investment appeal does not stem from direct participation in the AI compute race. Rather, it lies in providing the foundational connectivity infrastructure required to enable large-scale AI deployments. As hyperscale cloud providers continue to expand capital expenditures and build next-generation networking architectures, demand visibility across MaxLinear’s end markets continues to strengthen.

Arakawa Quant Multi-Factor Analysis and Investment Thesis Validation

Capacity Reservation Creates a Long-Term Competitive Advantage

Within the Arakawa Quant framework, MXL demonstrates exceptionally strong growth-factor momentum and favorable technical positioning. Near-term profitability, however, is temporarily influenced by proactive capacity reservation initiatives.

As the company prepares for large-scale product ramps, management has strategically allocated significant working capital toward foundry prepayments in order to secure manufacturing capacity during a period of industry-wide supply constraints. While these investments temporarily pressure reported profitability and free cash flow metrics, they effectively strengthen the company's future delivery capabilities and market share expansion potential.

In the high-speed optical communications industry, advanced manufacturing nodes and packaging capacity remain scarce strategic resources. During periods of accelerating demand, securing production capacity in advance often translates directly into higher fulfillment rates, stronger customer retention, and improved competitive positioning. Consequently, current free cash flow pressure should be viewed as a long-term capital allocation decision rather than a deterioration in operating fundamentals.

Improving Order Visibility Supports Higher Revenue Guidance

Driven by growing customer demand and continued design-win momentum, management raised its 2026 data center optical communications revenue outlook from a previous range of $100 million–$130 million to $150 million–$170 million. The company also guided second-quarter consolidated revenue to approximately $160 million–$170 million.

Importantly, this upward revision is not primarily the result of improving macroeconomic conditions. Rather, it reflects stronger order visibility, accelerating customer deployment schedules, and increasing confidence in future demand.

As a result, revenue growth over the next several quarters appears increasingly measurable and fundamentally supported.

Earnings Growth and Valuation Upside Remain Compelling

This acceleration has driven MaxLinear’s forward long-term EPS growth expectations to levels exceeding 418% above the median growth rate of the broader technology sector.

Although the stock has appreciated more than 500% over the past year, traditional valuation metrics may not fully capture the pace of future earnings expansion. When evaluated through a growth-adjusted framework such as PEG, MaxLinear continues to trade at a meaningful discount relative to several comparable AI infrastructure growth companies.

This valuation disconnect remains one of the primary reasons the stock continues to rank favorably within the Arakawa Quant multi-factor selection model.

Multi-Factor Confirmation Signals Institutional Repricing

In addition, the company scores highly across several key quantitative factors, including Growth Factor, Earnings Revision Factor, Industry Momentum Factor, and Price Momentum Factor.

From a quantitative investment perspective, periods in which earnings revisions, growth metrics, and price momentum strengthen simultaneously often coincide with major valuation re-rating cycles. MaxLinear currently appears to be operating within such a multi-factor convergence environment, suggesting continued institutional accumulation and market repricing potential.

Systematic Risk Assessment and Mitigation Bound

To ensure objective portfolio risk management, the quantitative framework balances structural upside against acute micro and macro risks:

Customer and Sector Concentration: MXL remains exposed to capital expenditure cycles within the traditional telecom and cable carrier markets. A slowdown in broader broadband infrastructure deployments could create localized headwinds.

Volatility and Liquidity Dynamics: The asset exhibits a high historical beta and remains sensitive to thematic semiconductor headlines, presenting drawdown risks if broader macro sentiment shifts. Concentrated institutional ownership can further amplify technical sell-offs.

Execution and Competitive Moats: Capturing market share in the Wi-Fi 7 and enterprise connectivity space requires flawless product execution against larger, well-capitalized mixed-signal competitors.

Conclusion

The investment case for MaxLinear is not built around a single product cycle but around the long-term expansion of global AI infrastructure.

As the industry evolves from a race for computational power toward a race for infrastructure efficiency, connectivity has become a critical component of overall AI system performance. For hyperscale AI deployments, efficient data movement is increasingly as important as compute itself.

MaxLinear should therefore be viewed not as a traditional semiconductor company, but as a strategic connectivity-layer beneficiary of the AI infrastructure buildout cycle.

Today, the company benefits from multiple reinforcing catalysts, including expanding AI infrastructure demand, accelerating optical networking upgrades, upward earnings revisions, institutional capital reallocation, and a favorable growth-versus-valuation profile.