Search All

Institutional Capital Insights: Navigating Market Breadth Shifts via the Arakawa Quant Multi-Factor Matrix

Executive Summary

Market Milestones: Major equity benchmarks achieved fresh historic highs during the first full week of May, fueled by expanding risk appetite, decelerating sovereign bond yields, and compressing crude oil premiums.

Sector Rotations: Technology and duration-sensitive sectors outperformed significantly as cooling inflationary fears sparked a capital rotation out of Energy, which emerged as the primary secular laggard.

Labor Macroeconomics: Nonfarm payrolls registered a resilient but non-inflationary expansion of 115K for April. Coupled with a steady 4.3% unemployment rate, the data solidifies consensus expectations for a soft-landing monetary regime.

Quantitative Outperformance: The Arakawa Quant multi-factor strategy continues to demonstrate significant alpha generation against the S&P 500, isolating companies with superior fundamental execution and forward earnings visibility.

Macro Briefing: Yield Relief, Supply Chains, and Soft-Landing Architecture

U.S. equity indices advanced to unprecedented record highs, supported by a constructive shift in structural macroeconomic factors and a material decompression of geopolitical risk premiums. A critical driver of this risk-on rotation was the cooling of supply-side inflation anxieties. Progress toward regional peace frameworks and the projected normalization of shipping logistics through the Strait of Hormuz forced WTI crude prices lower, removing a significant headline inflation catalyst.

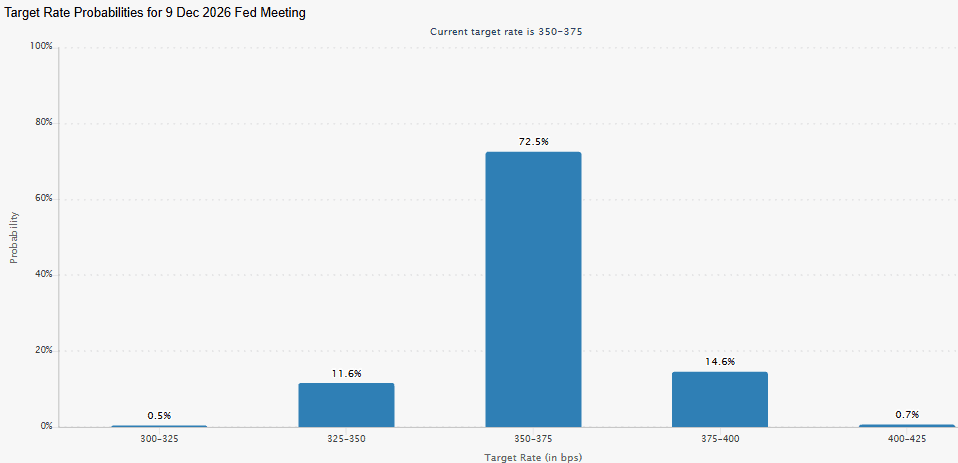

FedWatch Tool, CME Group, as of 12:00 pm, May 8, 2026

The fixed-income curve reacted aggressively to this easing premium. The benchmark 10-Year U.S. Treasury yield ($$US10$$) retraced from its intraday peak of 4.47% down to 4.36%. This decompression of the risk-free rate lowered equity discount rates, triggering a robust valuation expansion across long-duration growth assets. Concurrently, the sovereign debt market has adjusted its terminal policy expectations, with CME FedWatch metrics now fully pricing in a baseline expectation of zero interest rate cuts for the remainder of the 2026 calendar year, reflecting a structural commitment to patient monetary stabilization under the Federal Reserve.

This structural environment provided unique tailwinds for specific interest-rate-sensitive allocations. Technology (XLK) rallied nearly 5% on the week, while Consumer Discretionary (XLY) and Real Estate (XLRE) recorded notable capital inflows. Real Estate, in particular, capitalized on the stabilizing yield environment, which acts as an operational tailwind for asset-backed financing costs and commercial property valuations. Conversely, Energy (XLE) underperformed sharply due to the erosion of the crude oil cash-flow premium, while Utilities (XLU) lagged as compressed yields reduced the relative yield-spread appeal of defensive equity proxies.

The Arakawa Quant Multi-Factor Edge

In environments characterized by rapid macro rotations and shifting sector crowding, executing a disciplined, factor-based framework is essential to isolate behavioral noise from true fundamental alpha. The Arakawa Quant model systematically screens liquid assets based on five core mathematical pillars: Valuation, Growth, Profitability, Momentum, and Earnings Estimate Revisions.

By evaluating corporate execution and forward visibility through this quantitative lens, the portfolio has successfully sustained significant structural outperformance, delivering an absolute return of +389.27% since inception, compared to +93.79% for the S&P 500 benchmark.

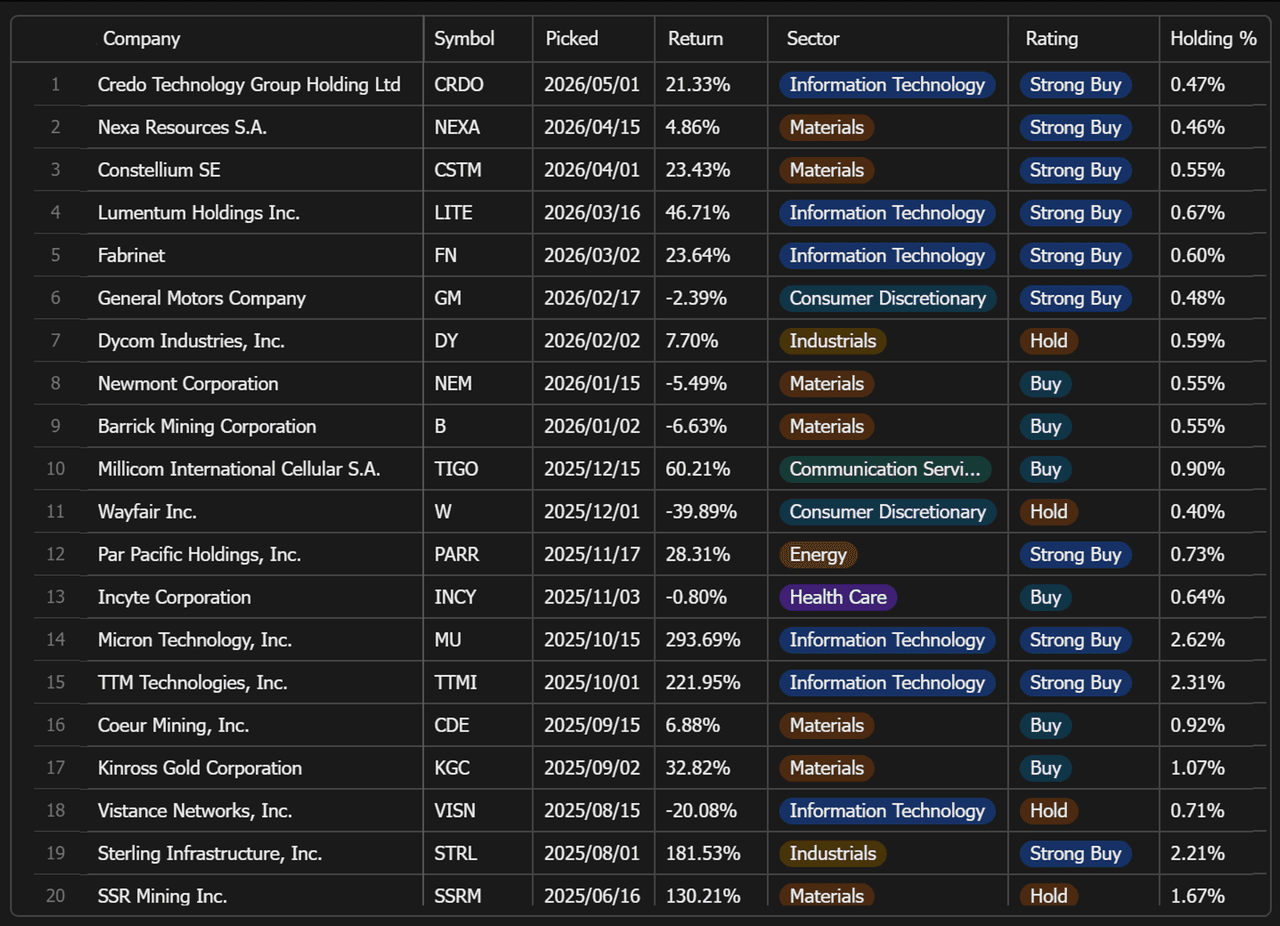

Factor Outliers and Microeconomic Drivers (Weekly Analysis)

Alpha Contributors (Strong Fundamental Execution):

Sterling Infrastructure (STRL): Surged following an exceptional earnings disclosure, reporting record revenue of $825.7 million and an EPS beat of $1.40 above consensus, confirming robust backlog visibility.

Twilio (TWLO): Gained on accelerating operating margins and renewed institutional confidence in its growth stabilization thesis.

Micron Technology (MU): Advanced on persistent high-bandwidth memory (HBM) semiconductor demand driven by hyperscaler AI capital expenditure.

SSR Mining (SSRM): Captured positive asset-allocation flows as gold prices rebounded alongside a softer U.S. Dollar.

AppLovin (APP): Accelerated on structural growth visibility within its software-based ad-tech engine.

Alpha Laggards (Profit-Taking & Guidance Normalization):

Arcutis Biotherapeutics (ARQT): Experienced downward pressure after soft quarterly earnings introduced near-term margin friction, despite steady commercial volume for its ZORYVE franchise.

Fabrinet (FN): Retrenched as in-line forward guidance triggered a technical sell-the-news correction following an extended AI-driven optical infrastructure rally.

Nexa Resources (NEXA): Consolidating as institutional desks locked in profits following a parabolic move in industrial metal spot prices.

Vistance Networks (VISN): Underperformed amid systemic de-risking within speculative, low-cap communications infrastructure plays.

Celestica (CLS): Underwent standard profit-taking as short-term technical indicators flashed overbought conditions following a major structural AI hardware expansion.