Search All

StoneX (SNEX) Monopolizes Commodity Risk Intermediation as Q2 Net Income Surges 143%

Executive Summary

Systematic Positioning: StoneX Group Inc. (SNEX) operates as a premier global institutional-grade financial intermediary, connecting real-economy commercial producers, mid-market corporations, and institutional traders to specialized liquidity networks often underserved by tier-1 investment banks.

Operational Inflection: In Q2 2026, SNEX delivered record-breaking fundamental acceleration, with total operating revenues climbing +64% Year-over-Year (YoY) to $1.6 billion, and net income surging +143% YoY to $174.3 million.

Framework Return Verification: Backed by persistent macro volatility and cross-border structural flow growth, the core Arakawa Quant multi-factor strategy framework continues to achieve robust capital appreciation, tracking at +421.61% since inception in July 2022, compared to +96.50% for the S&P 500 benchmark.

Asymmetric Valuation Corridor: Despite delivering a trailing one-year absolute return exceeding 119%, the asset maintains a severe multiple discount relative to the financial sector median, presenting a compelling valuation disconnect as consensus models materialize.

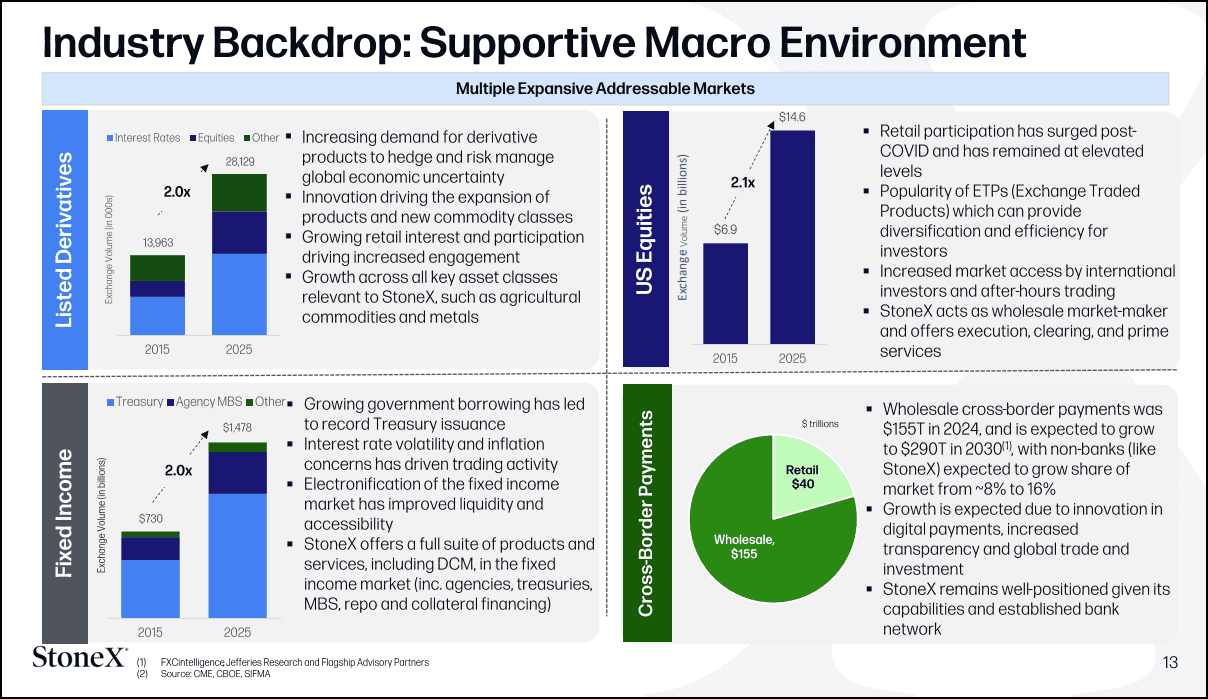

Macro & Business Architecture Analysis: The Non-Bank Flow Aggregator

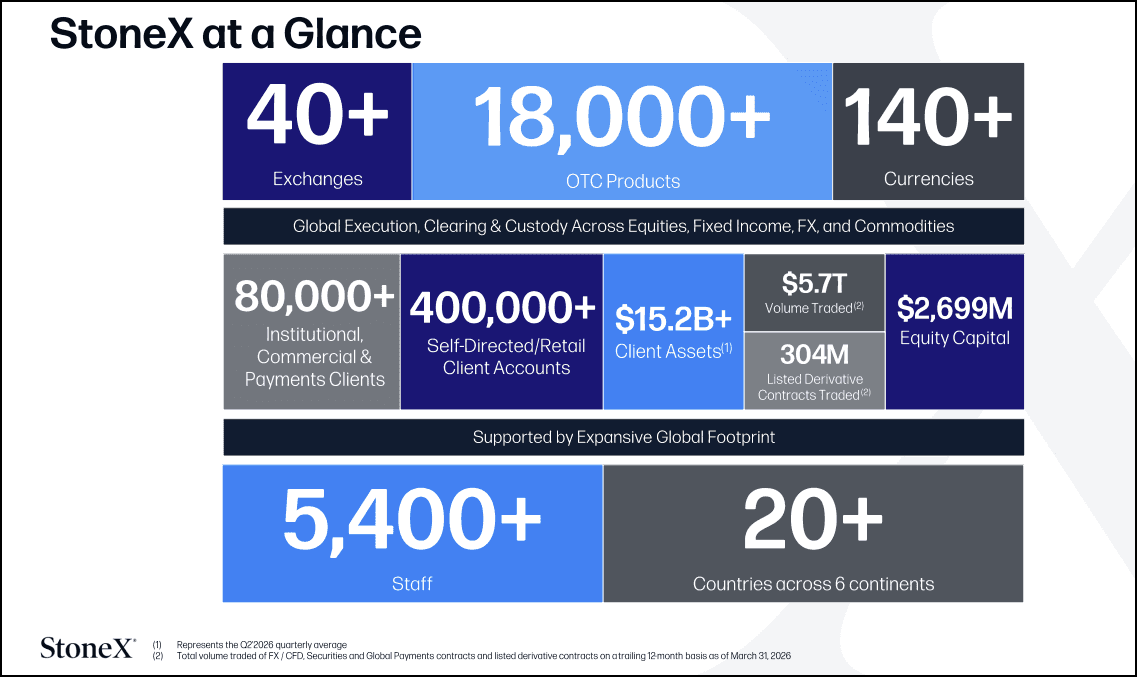

Within the Arakawa Quant financial sector allocation engine, StoneX Group is structurally isolated not as a directional directional risk-taker, but as an indispensable transaction-flow and hedging utility. The firm's business model is explicitly engineered to extract recurring spreads, execution fees, and net interest income from real-economy volume flows across listed derivatives, OTC cleared contracts, physical commodities, and FX cross-border payments in over 140 currencies.

SNEX Q2 2026 Investor Presentation

A core structural advantage is the sticky nature of its commercial client base—primarily agricultural producers, mining entities, and mid-sized enterprises utilizing customized OTC derivatives to manage physical price risk. This configuration builds high switching costs and creates counter-cyclical resilience: heightened market volatility and inflationary uncertainty directly stimulate corporate hedging velocity, lifting clearing fees and capital spreads simultaneously.

Furthermore, the post-merger integration of R.J. O’Brien has successfully solidified StoneX as the largest non-bank Futures Commission Merchant (FCM) in the United States, positioning the enterprise to capture up to $50 million in run-rate structural synergies.

Arakawa Quant Multi-Factor Matrix Alignment

The asset demonstrates an institutional grade profile across core growth and capital efficiency pillars, characterized by an under-followed analyst coverage base that yields significant pricing inefficiencies.

SNEX Q2 2026 Investor Presentation

On a systematic factor basis, SNEX presents a premier combination of value and momentum. Q2 FY2026 performance underscores this momentum, with the Commercial operating segment expanding net operating revenues by 111%, fueled by a 98% jump in customized OTC structures and a 162% surge in physical contracts (predominantly precious metals). The Institutional segment concurrently scaled average daily securities volume past $12 billion.

Financially, net interest and fee income earned on expanding client float balances grew 54% to $154.5 million, providing a highly predictable baseline revenue anchor. With year-over-year and forward EPS growth metrics pacing 147% and 65% above the sector median respectively, the asset's valuation remain deeply depressed. Trading at an 84% discount on a trailing price-to-cash-flow basis relative to peer institutions, the equity is poised for structural re-rating, further supported by enhanced liquidity from its recent 3-for-2 stock split.

Systematic Risk Assessment and Defensive Boundaries

To enforce rigorous capital preservation, the quantitative framework establishes clear risk parameters:

Counterparty Credit and Margin Volatility: As a central clearing intermediary, extreme market gaps can expose the firm to systemic margin-call defaults or collateral shortfalls if commercial clients experience localized hedging breakdowns.

Cyclicality of Volume and Rates Regime: A macro transition toward low-volatility regimes or aggressive central bank rate cuts could compress both transaction-fee velocity and net interest margins on client float.

Scale and Technology Competition: Sustaining market share against automated electronic brokerages and mega-banks requires continuous capital expenditure into internal clearing software and cybersecurity infrastructure.